Whenever or do we ever discuss the CPF system with friends and family. The actual fact is that I never really do unless it is time to do something about it. That involves tax season or even property tax season. I do feel that it is a system that we think we all know but once we delve deeper, there’s always something new to takeaway.

Let us also face it. It is a dry topic and a very long-term one. It tries to mimic a pension fund of some sort with some level of control yet it works differently for different people. I can understand why some people come to dislike the policy but in general, there’s not much hate around it. We also have to be factual that Anti-government does not mean you need to be anti-CPF. Some might differ but I think all tools that bring one to the final goal are the ultimate endpoint.

Contribution rates according to age and wages

The rules are pretty simple. Understanding that before 55 years of age, all employees have to contribute 20% of their gross salary. Subject to the ordinary wage cap which we have discussed previously.

After 55 years of age, the contribution starts to decrease. This makes sense since the decrease in employer contribution, older employees will become less expensive and it helps to make employment more affordable.

After 55 years of age, the OA and SA will be combined and set aside in one’s RA to safeguard a monthly payout in the later years. This is probably why the contribution rates start to decrease then. Further, with increasing age, the focus will be more on wealth preservation and income that can be utilized. That would be the next reason why the contribution is lesser as time goes by.

Contribution by age from the CPF website

Understanding the CPF – Did you know? What contributes to your CPF?

Understanding that CPF system – These mainly include all forms of payments that are paid out to the employee by the employer.

Basic Wages

Overtime Wages

Bonus

Cash Incentives

Commissions

Cash Incentives

Understanding the CPF – Did you know? What does not contribute to your CPF?

Termination/Retrenchment Benefits

Reimbursements

Benefit in kind

Disclaimer

If you like what you are seeing, do remember to check them out and do your diligence. There is no one-size-fits-all investment strategy and no one solution to life. Join my telegram group to find out more about deals and join the community to connect for ideas: Life Journey Telegram

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral Services

It is very interesting to know that many people are interested to know about the CPF. Hence, I’ve decided to do a simple part series that focuses on selected and focused information so that it doesn’t take too long to read and understand. In my previous CPF series, we discussed the increase in CPF contribution on Ordinary Wages aka Salary.

CPF is a complex retirement module indeed and it has different accounts. CPFIS in turn has its pros and cons. One needs to understand it to use it to your own advantage. Most of these come at retirement as a motivation or tax deductibles. That said, it works differently for everyone so good to be in the know. One can be anti-government but we should applaud a strong and stable governance. This in turn will relate to a trusty CPF system not everyone can replicate.

Types of CPF account and what they can do

Ordinary Account:

Be happy retiring and be happy doing what you do when you retire

Though CPF is restrictive OA is the most flexible out of all three accounts before one turns 55. This is the account that one can use to invest a portion into selected CPF-approved investments (CPFIS), gold, approved insurance, and also property payments. One can look at index investing using a Robo Advisor of some sort. such as Endowus or StashAway. Endowus ticks a little better for me for the investing portion. If we look at the iShares US index Fund S&P 500 that Endowus offers to track the S&P500 (100 years of historical performance). I also have my funds consistently invested in them and it has worked well. What I really like is that they care about who invests with them and the fees.

You can check them out here at Endowus or in my previous posts which I slowly grew to like over 2 years. Asset Allocation does not time the market and during times when I’m distracted, I do not need to log into my app to proceed with my own adjustments or take action. (These take time and effort)

Asset Allocation

Special Account:

This account builds the Retirement account that will eventually be used in the retirement account in the form of an annuity. More restrictive than the OA, it has limits and can only be utilized for retirement-related financial products (Nothing much can be done in this account) It is also known that OA can be transferred to MA – This is well known to be irreversible once you have done so. Do consider your circumstances before you do anything)

Medisave Account:

This is the most restrictive of all and as it states Medisave means it can be used for certain medical payments with a limit. The MA account is also allowed to be used to purchase medical-related insurance.

Retirement Accounts

Retirement Account:

This account is non-existent until you reach 55 years of age at the point of writing. This is the combination of your OA and SA to form the annuity payout.

There are also many ways for one to contribute to your own CPF accounts. I’ll say it is a good problem to have if you need to think of fresh ways to contribute to your own CPF funds. (i.e. self-employed and looking for proper and forced retirement). Side note that CPFs are monies that are locked away in the form of something like a trust so one can’t claim your assets in your CPF (If for some reason, you are locked up in a situation of some sort)

Some ways to look at contributing to your CPF accounts

Make cash top-ups or Top up Cash + CPF

Your OA, SA, and MA – through these cash top-ups, you can earn interest. Note that these are long-term retirement uses.

Can’t say that too many times if you want to do forced savings.

Matched Retirement Savings Scheme (MRSS)

If you’re 55 to 70 and have yet to meet the current Basic Retirement Sum (BRS), you can make cash top-ups to get higher retirement payouts. The Singapore Government will match every dollar of cash top-ups made to your RA, up to a maximum grant of $600 a year. The scheme will run from 2021 for five years for a start. (Taken from the CPF website)

Helping your parents or in-laws with the CP scheme helps you and the older folks as well.

Invest your OA savings

We discussed the option of investing in a wide range of investments to grow your retirement nest egg in the form of the CPF Investment Scheme which is very highly restrictive.

As for SA, you can invest in those too but even more restricted.

Voluntary Housing Refund

If you have used CPF to purchase your house and have excess cash. One way is to kind of payback voluntarily. However, recently the cash returns outweigh that of CPF returns so with careful management, it does seem like it is better to hold cash but it is a better yielding instrument for now.

Too complicated? Leave it as it is and put the cash via this method to earn that CPF consistent return.

For CPFIS/Investing – The reason for Endowus

Like a broken recorder, why do I like using them for now:

Endowus is the first and only robo-advisor to be approved by the CPF board.

100% trailer fees back to the consumer, not the fund management fee. This is really one of a kind I’ve seen so far.

They do have a decent team that makes sense when introducing their platform in my personal opinion.

I believe all retail investors should try them out because of how they are trying to disrupt investing and make investing work for everyone.

If you like what you are seeing, do remember to check them out and do your diligence. There is no one-size-fits-all investment strategy and no one solution to life. Join my telegram group to find out more about deals and join the community to connect for ideas: Life Journey Telegram

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral Services

Happy 2024 everyone! Everyone knows 2024 has a staggering change in CPF and the government has done that to help businesses to adapt. It is strange though that the last post about CPF had a bit of viewership. Perhaps the interest in CPF has really changed over the years.

Last Sep 2023, the salary cap (OW) was increased to SGD 6,300, and from 2024, there will be an increase to SGD 6,800. What that means is that more of the money that you earn goes into your CPF aka retirement account every month. Your employers will also have to contribute more to your CPF. I can’t say if that is a good or bad thing.

I guess we are touching on a sensitive part of everyone’s life. Your Salary. Salary are always a sensitive part of most people’s discussions. However, these are all hard truths that we have to come to terms with. Some people do have that special negotiation skill to make more while doing the same thing. We just have to work more productively.

Sidetracking a little, everyone is a salesperson to themselves so don’t say that you don’t do sales. When you go for a job interview, you are selling yourself for the package that you think you are worth. You will need to justify your costs to the hiring manager.

Back on track again, today we are focusing on the monies that go to your CPF. Regarding the monies on CPF, please note the statement on the CPF website that states that:

(a) The CPF Ordinary Wage (OW) ceiling limits the amount of OW that attracts CPF contributions in a calendar month for all employees. The OW ceiling will be raised from $6,000 to $8,000 by 2026, with the first increase to take place on 1 September 2023. The increase will take place in four steps to allow employers and employees to adjust to the changes.

This means that the changes are made to let business manage their cashflow instead of a bang…a 2k addition to employers’ contribution and less take-home pay for the employee (Since 2023 costs, inflation, and goods have all increased)

(b) There will be no change to the CPF annual salary ceiling of $102,000, which sets the maximum amount of CPF contributions payable for all salaries received in the year, inclusive of both Ordinary Wages and Additional Wages.

This actually means that people who have more resources than the rest will not be able to game the CPF. This is pretty fair in my opinion since this is a tool to help Singaporeans whether they have little or a lot more resources. However, the truth is also that when you have more, there’s more that you can do that others can’t. The only takeaway is that the rich get richer but only at a cap.

(c) There will be no changes to the Additional Wage ceiling and CPF Annual Limit, where they will remain at [$102,000 – Total Ordinary Wage subject to CPF for the year] and $37,740 respectively.

Same points as (b) above. There’s that cap that restricts more from getting more if you know what I mean.

I’m quite sure everyone is aware of this but probably left that somewhere. I’m just bringing it back since the changes took effect this year. I took this off the CPF website where the Salary OW cap process will happen.

Just a disclaimer that everyone’s situation is different here so it is important to stay in the know so that you can plan your finances in advance. As the saying goes, if you fail to plan, you are planning to fail:

This is something one cannot control. Employee or Employer. We can only embrace the change.

Let’s look at it positively. This will compound interests for many and help build or supplement the CPF retirement nest.

My thoughts are that this actually does hurt business owners a little more. Over time, these staff costs will indirectly translate into services, items, goods, and whatever is sold to consumers or businesses.

In my next CPF series, I will share or talk about CPF programs and how to help your parents or elders who do not believe in CPF (Or rather too complicated to understand) You just don’t reject free money.

Disclaimer

If you like what you are seeing, do remember to check them out and do your diligence. There is no one-size-fits-all investment strategy and no one solution to life. Join my telegram group to find out more about deals and join the community to connect for ideas: Life Journey Telegram

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral Services

On 4 November 2022, 3 working days after OCBC rolled out their new interest rate on their flagship 360 accounts, DBS followed up with an email that the DBS Multiplier has increased from 3.5% to 4.1%. The balance cap amount is also increased to S$100,000

The Multiplier account has always been proportioned by the transaction amount.

below S$2,000

S$2,000 to below S$2,500

S$2,500 to below S$5,000

S$5,000 to below S$15,000

S$15,000 to below S$30,000

Above S$30,000

The next layer of categories to fulfil will be the number of categories. They are known to be:

1. Salary/Dividends/SGFinDex

The Salary portion has to be a GIRO transaction with code “SAL” or “PAY”, which seems pretty strict given that there are increasing numbers of the next generation in the ‘gig economy’

For dividend crediting, these eligible dividend has to be from CDP, DBS Vickers Securities, DBS Online Equity Trading, DBS Unit Trusts, DBS Online Funds Investing and Invest-Saver (Promotion their own eco-system)

Connecting and sharing financial information from SGFinDex to NAV Planner (I would think one needs to do this on a monthly basis

2. Credit Card Spend

For the monthly card spend, it has to be on any DBS credit card and has to be eligible spending. Eligible will be the usual suspects and it will be very much dependent on the MCC codes.

3. Home Loan Installment

Home Loan financing has to be from DBS or POSB (New or Refinancing). The eligible amount will be from the monthly home loan instalment amount.

4. Insurance

Similar to my previous post on insurance and investment in these high-yield accounts. These are usually valid for a limited period and interest rates are always subject to changes. Further, only selected insurance are eligible.

5. Investment

Nothing much to comment on here. This section will be pretty hard for most people to fulfil.

Additional option: The PayLah! Retail Spend. Honestly, don’t seem like a good deal to me.

The ideal interest rate will be between 0.9% to 2,5%. Frankly, nothing much has changed though and I don’t think it is even worth announcing via their communication channels. I feel like there wasn’t even much thought placed into it. I just felt like it isn’t any effort to compete with these changes. With the most recent 0.75 bps increase by the US Feds, this is not anything competitive and not quite worth looking into for now.

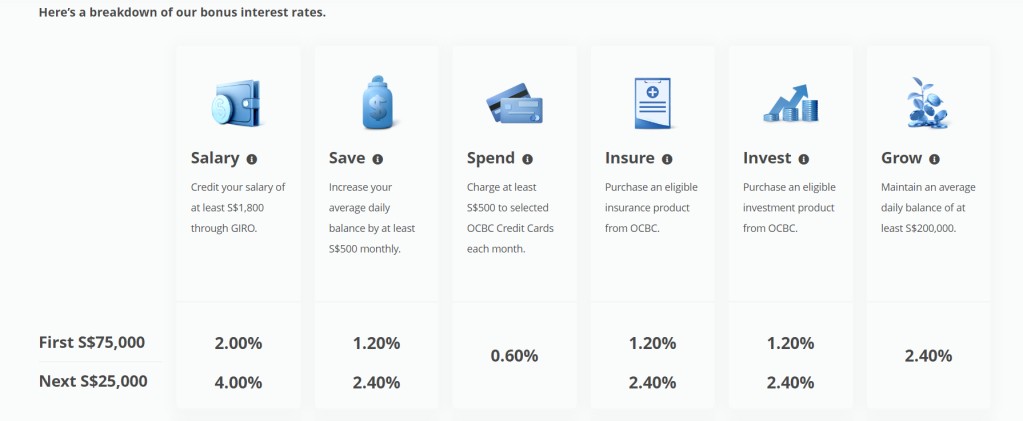

The week has been intercepted by headline interest rate hike news and OCBC 360 certainly did take out their competition with a banging headline. As of the 1st of November 2022, the entire suite of the OCBC 260 flagship account will revise its interest rate across the board.

As of their online quote, “The OCBC 360 Account has six bonus interest categories – Salary, Save, Spend, Wealth (Insure), Wealth (Invest) and Grow. By tapping on just three of these categories – Salary, Save and Spend – customers will be able to earn interest of 4.65% p.a. on the first S$100,000 in their bank account.”

Prior to this due to the interest rate environment, the first S$100,000 could get you 1.85% p.a. The biggest update is that for their spending options, you can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

There are a total of 6 categories:

Salary, Save, Spend, Insure, Invest and Grow.

The basic of the high-yield account is to fulfil the following – Salary, Saving (Keeping the average daily balance by $500 increment monthly) and spending S4500 to the above-mentioned OCBC credit card each month. Quite simply put, by fulfilling these three options, your interest yield is 4.65% p.a. for up to $100,000. (technically 4.64962903% p.a.)

Over 365 days, the interest earned is S$4,649.63

Salary

You need to credit at least S$1,800 of your salary to fulfil the Salary Category. That is if your HR allows that or if you are not employed in another rival or financial institution.

Save

You need to have an incremental S$500 in your monthly balance. However, if this is your transaction account then it might be an issue. But as long as it is an incremental (Average daily balance)

Spend

You need to spend S$500 on selected OCBC credit cards. You can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

Insure & Invest

Forget about the insurance and Investment portion, there’s probably no way around those.

Grow

For the Grow category, if you have an additional S$100,000 to keep the average daily balance of S$200,000, the first S$100,000 will get an additional 2.40% p.a. while your remaining S$100,000 remain at the 0.05% p.a.

To illustrate, the interest over this S$200,000 will be S$7,099.60 hence the yield for this amount will be 3.55% p.a. (technically 3.54980161% p.a.

To calculate your interest amount, use the link to calculate the expected interest on your saving amount here: Calculate your Interest Amount

Conclusion

This is very interesting indeed. Because competitors will drastically make these changes as well. The interest rate hike might be a good and bad thing. However, take note that these rates are never confirmed or fixed. They follow the current market conditions. By taking on investments or insurance, these interest rates might change fast and furious. Overall, valiant effort and quite good timing as well. In the next few weeks, we might see revisions to compete with this increase in interest rate.

Whenever we touch on the topic of CPF, also known as Central Provident Fund (Pension Fund – The Europeans and Americans call it), people get kind of edgy and upset. What I do observe is that mostly a certain group of people is really anti CPF. The first group is those who are anti-government, not fueling anything here but just a general consensus. The second group is the retirees or about to retire folks who didn’t have a decent education (At that point in time, it wasn’t necessary to have the paper qualifications) and the last group is the self-proclaimed Warren Buffet who claims to beat the market.

The Central Provident Fund

The CPF in my opinion, is something of a great system. There are certainly flaws to it but in my view it is the perfect, AAA grade, higher yield returns that can supplement all our retirement fund. There are certain risks but There are no investment tool has no risk in reality. I finally conclude that as a result of these 3 group of people, these are the reason why so many people dislike the CPF system.

The AAA rating

a. Unfortunately, it is a complex system – You need to read up and understand how it works to appreciate the system

b. Inflation rate is here to stay hence the increase in the minimum sum yearly

c. No one is taking your money away.

d. No. There is no crystal ball. Statistically, it is proven that you can never win 100% of the time. Anyone who have tried or attempted to invest their monies will know that there is no clear strategy out there but a lot of hard work so you will not be able to beat the benchmark all the time.

e. Good quality investments and yields are hard to find these days. Perhaps it is a reality check and time to reflect about strategies as well as accepting facts and the markets

Understanding what CPF is about

When I first explored CPF, it was when I was out of school into my first job. At that time, CPF seems like a Goliath – You think you know but eventually, you slowly find out stuff which you never know before and for a long period of time I put off reading up more about them. It was many years back that I started reading financial blogs and it became like a ritual. I’ll do that almost any other day.

Back in those days, there were less bloggers so you will still need to dig deep to find out how stuff works. Then came Technology advancements, social media and super apps/content apps. I also discovered a few more bloggers who actively shared about CPF. One one those whom I follow really closely is 1M65. His is a well-known blogger for CPF and he developed his own strategies around what the CPF has been doing for many years.

Life Cycle

1M65 is really about having a million in your CPF by 65 years old. Depending on how you look at it, he is preaching a 4M65 these days and base on his concept – I do think that is possible if you start really young. Anyway, his idea about have these sum of money is really to get you thinking about your own retirement early, not just when you are in your mid stage or even late stage of your life cycle.

Everyone is different

Most importantly, everyone is different. There is no need to look at it in the form of a showboat or saying that it is impossible. Being open and understanding how these people are doing do help yourself to be ready for retirement – You are doing your next generation a favour so that they will not fall into the sandwich class or fall in the same cycle again and again. Of course, teaching the value of money to the next generation is something that needs to be worked on as well. It’s not like they were given a sum of money to deal with in life.

Some people actually worked two jobs or even saved excessively so that they can put all their money into retirement. Again, lifejourney preaches about having your own quality of life. If you need to feel like you have to give up everything just to be thrifty (It is a really thin line to term it as miserly), then you would most likely have to re-think your strategy.

The Practical Approach

There are a lot of concepts that you can read about but most of them come from a theory. Personally, I don’t really like to dissect those as they are so technical and heavy. Most importantly, it is extremely boring to put them down in words and executing them is really the best way to practice

Stock market digital graph chart on LED display concept. A large display of daily stock market price and quotation. Indicator financial forex trade education background.

As 1M65 says, you can hate who or whatever but don’t hate free money. Initially, it sounded like a money grubber statement but eventually I came to realise that, it is really free money. If you have no plans to be an entrepreneur, there is a few things you have to take note of in CPF. Yes, I am sorry but everything has to start from the basics.

My View on CPF

a. My biggest take on CPF is to compound the interest. The more you have, the greater the growth. The younger you fill up your CPF account to accumulate interest, the faster and bigger your pension fund will grow.

bi. If you are below 55 years of age – Your first $60k in CPF will gain an extra 1% p.a. (This is capped at S$20k in your OA) The current base Ordinary Account (OA) is 2.5% (3-month average of major local banks’interest rates, whichever is higher)

bii. For most people, the next S$40k will most likely be in your Special Account (SA). For others who are still building your SA, that will be whatever that is in your MediSave Account (MA). The base rate for your SA and MA is at the current floor of 4% p.a. (which is also the 12 month average yield of 10-year Singapore Gov Securities – 10YSGS)

My Tips:

Your CPF interest is computed monthly based on the lowest balance for the month. This means that for interests paid out on your CPF accounts in Year 2020, the interest amount is based on what was captured monthly, compounded and only paid out to you in full before 1st Jan of 2021.(This is subjected to changes if you have transactions every month)

c. As much as possible, you have to try your best to hit the minimum sum as early as you can. (Combined OA and SA) Once you manage to do that, you do not need to worry about the annual increase in minimum sum that is subjected to inflation.

My Tips:

Don’t lose faith if you have not or still very far from this. Everyone starts from $0. Let the small actions and do up your checklist one by one in order to build the financial confidence. Everyone is different – it is the end goal that matters.

d. Depending on your circumstances, you can choose to invest your CPF OA money after the S$20k accumulation. Similar to cash, have a long term goal and build your portfolio. Good companies and investment ideas doesn’t come easy. You have to make sure what you invest is more calculated risk. There is a risk to everything.

My Tips:

Don’t be affected by market noise. My tip is to buy when there is a price drop if the investment moat for the company still makes sense. (but always do your own diligence) You can also have different pockets of funds so that when there are opportunities or if there is a correction, you can be ready to enter the market. The rule is to always stay invested.

Summary

In Summary, CPF is not the perfect solution but a supplement of your retirement goals. In this aspect, we are responsible for our own money and retirement. No one else will take care of your money as much as you will do. Only you will know your own financial situation. The question is to ask to meet these financial goals is that if you can cut back on your lavish lifestyle or even saving more to add to your pool of funds. No one can coerce you to do what you do not wish to.

Disclaimer

This is not a sponsored post. This is purely my own opinion about CPF and retirement. If you like what you are seeing, do remember to check them out and do your diligence. There is no one size fits all investment strategy as usual