I have been later for one quarter in 2021 in terms of updating. Nothing much has changes for the StashAway portfolio. Similar to Endowus, it is on auto-run and monthly additions are placed into different portfolios. I am still on the risk index of below 20%, split all the risk portion for 3 different portfolio. I still maintain that having calculated risk per $ makes more sense in my opinion. It doesn’t mean high risk high rewards although it can give you high rewards.

As I have always preached, the important thing is that I am not left on the sidelines. If Mr Market decides to go either way, it would matter that much to me in my opinion. If Mr Market drops, then I will add on more to the portfolios. That is what I believe will work for me for my traditional and rather stable investments.

Retirement Portfolio A (risk-14%)

The SRS account since deposit is currently at +2.11% as on 8 Apr 2021 (Time-weighted return). I think this is quite okay as I entered the market at a high before it dropped in March 2020. Performance wise, I think it is decent and also this is a super long term portfolio – I would say close to 25 years horizon so I’ll just leave it there to monitor on the progress. It was at around +3% in Dec 2020 but oh well. Let it be i guess.

In USD performance, that’s about 5% (Time-weighted return). That’s expected.

Education Portfolio B (risk-16%)

This portfolio is set out to be on a 15-18 year investment horizon. It is at 7.63% on 8 Apr 2021 and I think that this is pretty good. It’s the same as the last time i measured during Dec 2020. I have been averaging in whenever there are market dips. The risk index is at 16% and I will adjust those risk levels as and when I feel that there is a risk on or off.

In USD, I’m looking at double digits 11.75% (Time-weighted returns)

Education Portfolio C (risk-20%)

For this portfolio, I look at this at shorter horizon of 12-15 years so I feel that I need to take on some risk to achieve my goals. This SA risk index is currently at 20% and will take on to be one of my riskiest portfolio. Return is at 14.42% (Time-weighted return) at inception as at 8 Apr 2021 Not much of it has changed or rather it has dropped slightly but this is just a note to self and measure the monthly performance. Over time, more funds will be added to achieve the targeted invested goals.

In USD terms, we are looking at 18.81% (Time-weighted return). Looking great I feel.

Conclusion

So far StashAway has been a great supplement as a robo advisor. I will try to do more regular updates as a reminder to self. After using a few robo-advisors, I find that SA will play second fiddle to my Endowus Portfolio. The year of 2021 should be a test of time for most portfolios. I still believe that rebalancing regularly will be the key.

StashAway does have their own advantages. They do hedge their portfolios against huge crashes and take a stand on some positions which I do like because a lot asset managers don’t and even though they talk big about macro. I can’t see those actions being translated into customer’s returns.

To sign up or try out Stash Away, visit the website and use my referral code at Stash Away Referral

We’ll both get up to $10,000 SGD managed for free for 6 months which is a good deal.

Disclaimer

If you like what I am sharing or if it resonates with you, do use my referral codes for other services at Referral and Recommendations

The pictures were taken from the Stash Away website for this article.

Investing especially in spot market is a tough business. Most people cannot accept fluctuations in their portfolio. Autowealth is yet another solution for me. Just that this time around, this is for my kid to start out her investment journey when she can. Teaching financial literacy is something I would recommend to anyone.

Summary on my review on Autowealth:

(a) try out different more robo advisors to understand more about them and how they invest and

(b) segregate this fund for any other purpose other than the kid’s investment journey.

My take about the investing journey has been the same since day one. Don’t sweat the small things, the costs of robo are so low. We are talking about a 15-20 year horizon here so heck those low costs. You need to pay them to keep their lights running. For companies like Endowus and StashAway, these guys have the experience and passion and these translate into actions. I am satisfied on how they are prudent and still maintain the low fees.

In my previous performance to compare the performance, I discussed about the historical S&P 500 chart for the last 50 and 100 years. Markets will go up and each time it drops, just pick some up and let the robots do the work on balancing and re-balancing. As long as fees remains low, the portfolio will grow over time and over a longer period. It should remain in the black based on some backtesting.

Performance

Looking at the portfolio again in November, it still looks pretty nice ahead of the 15-20 years horizon. This is a portfolio which is set at roughly 40% equities and 60% bonds. The investment vehicles will be through ETFs. It does look like it can withstand long term peaks and troughs. What i really like is that i can switch between the SGD and USD currency performance portfolio as well as the impact on USD SGD forex on performance. I wouldn’t say this does as well as the portfolios but to be fair, markets were already slightly upwards and I would like to deploy funds out into the market in tranches over time.

As compared to October 2020, +5.66% absolute is decent in my view (that is +2.66% comparing to October) and this is as at 11 Dec 2020. If markets drop, the rule is to fund the account more. Do note that all of these will have USD exposure. Time versus DIY – it is really about what is important. I usually will want to see the ultimate end goal whenever I start anything.

For this month, I also tried to look at the impact of FX and without the weakening USD, performance in USD is actually 8.56% year to date. That is on course to double digits returns once more.

The impact of the USD FX exchange is actually affecting the performance by -3.1%. These FX risks are part and parcel of investing unless I just intend to invest into the Singapore Markets. However, it is just too boring to do so.

Disclaimer

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

If you like what I am sharing or if it resonates with you, do use my referral codes here at https://atomic-temporary-178675883.wpcomstaging.com/contact/ for the services.

The pictures were taken from Auto Wealth website for this article. If you need a referral code, drop me a message and you can indicate my full name during registration. From there, both of us will get $20 each to supplement the fees.

Here comes another Robo-advisor experience from my end. To re-iterate the risk level, I am still at the risk index to below 20% as I felt that there isn’t a need to go all out Risk On going into November. I still think that having calculated risk per $ makes more sense in my opinion as news and information goes on a random rampage.

As I have always preached, the important thing is that I am not left on the sidelines. If Mr Market decides to go either way, it would matter that much to me in my opinion.

Retirement Portfolio A (risk-14%)

The SRS account since deposit is currently at +2.07% as on 11 Dec 2020. Pretty stagnant I would say but I’m not too worried about this long term portfolio. Performance wise, I went into this knowing it was pretty high end of Jan 2020.

Education Portfolio B (risk-16%)

This is something I set on a 15-18 year horizon. It is at 5.78% on 11 Dec 2020 and I think that is okay going at around 6-7%p.a. that I assume going into the end of 2020. I have been averaging in whenever there are market dips. The risk index is at 16% and I will adjust from time to time but try not to touch any of those if you don’t quite understand how that works.

Education Portfolio C (risk-20%)

This portfolio has a shorter horizon of 12-15 years so I feel that I need to take on some risk to achieve my goals. This SA risk index is currently at 20% and will take on to be one of my riskiest portfolio. Return is at 10.14% at inception which I find it fantastic to reach double digits. More funds will be added over time to achieve my targeted invested goals.

Conclusion

So far StashAway has not failed me in a sense that it fits in to my investing style and logic. I wish to put more into the accounts but I can’t bring myself to invest when prices are going higher. However, this is a pretty good supplement in my opinion.

I shall re-look into how I present the performance. Perhaps a more systematic approach so that it is more of a reference instead of just a monthly update.

a. Month on Month

b. Quarter on Quarter

c. Year on Year

To sign up or try out Stash Away, visit the website and use my referral code at Stash Away Referral

We’ll both get up to $10,000 SGD managed for free for 6 months which is a good deal.

It is the time of the month again. I must say I have been really satisfied with the way it Endowus has been working out well for me thus far.

November has been a quiet month. The portfolio makes diversification much more important. As I have always said, being systematic about investing is quite important. Month on month and it still fulfills what I am seeing so far. This is going to be one of my core robo-advisors that I would like to be on for the long term.

SRS Portfolio

Overall, portfolio is up 4-5% month on month in terms of SGD. In USD terms, due to no FX impact as the portfolio is USD ETFs, the performance will definitely be better. We are spending Singapore dollars so this is our reference currency. This is the SRS/Cash portfolio which consists of my favourite Dimension Funds in a 40% bonds/60% equity. Overall from May 2020 to 11 Dec 2020, it is a 11.30% increase in absolute terms.

CPF Portfolio

For the CPF portfolio, it does not come with the Dimension Funds due to the restrictive nature in what you can invest in but I think this is excellent performance compared with the 2.5% in CPF.

Month comparison from Oct to 11 Dec 2020, that is 9.32% in absolute returns ever since investments were made in May 2020. and comparing the previous month, that is estimated to be around 3% higher.

This is very good in my own opinion that I have not been doing anything to this portfolio.

Recently they came up with a SmartFund DIY portfolio which looks really interesting. I would definitely be looking this up when there is a market pullback like i mentioned last month.

A quick review once more:

Endowus is the first and only robo-advisor to be approved by the CPF board to use your CPF OA excess funds to invest.

100% trailer fees back to the consumer, not the fund management fee.

Content and education still remains relevant at least in my opinion.

At least they are one of the robo I trust that wants to help retail investors.

I realised that such posts actually attract more viewership as compared to technical breakdowns. I get it that most people want a quick and fast way to read content and download views. The first 3 seconds of every post will most likely decide if the reader would like to continue reading, be skeptical or just scoff at it. In my earlier posts, I talked about having an emergency fund. It takes time to build such things so don’t forget, the little things count.

In this article, I’m going to discuss more about what to invest and why especially for folks who just got out of school. When I graduated, I remember vividly that it seemed to be pretty hard to save money. A few years on, I realised what constituted the bulk of my spending and why I could not save more. These life experiences cannot be bought so I would say the money spend networking and forging friendships are my human capital.

Going back in Time

Going back to 5 years ago, there wasn’t many choices to invest extra funds into. It was the standard brokerages, fund houses or at most bank/custodian brokerages. There wasn’t a lot of tools to invest in and let’s be honest, the retail bankers can’t be too bothered with a S$10,000 fund. It just isn’t worth their time. So, like many others who preaches, I shall say it again – If you do not care about your own money, no one will. I remember I used to buy funds via FundSupermart, trading some Forex with CMC Markets/Saxo Capital and used Standard Chartered Brokerages to buy US/SGD equities. Nothing fancy that you can really do though.

Moving forward 2020

With the current options we have available, traditional investments seems really cool. (At least it is for me) I really like the options out there for me to pick and choose. You can Insurance Tech, Robo Advisors, Cryptocurrency, Real Estate Block-chains, ETFs, Leveraged Equities/Indexes and many more. With the upcoming digital bank in Singapore, I think that this is going to be great for consumers. The key problem now is to get more people interested in their own personal finances.

What to do with S$10k?

We are going to take away the cash solutions for this since this is on the assumption that cash funds are kept away in a safe place. With the new funds, this is money that you can afford to lose. I used to know something who likes to take a punt, he would leverage and buy options on the same counter without considering the risk. Well, he wanted to win big but eventually his portfolio became pathetic and he lost his job while these options expired and markets dropped. The objective of sharing this story is to always abide by your investment discipline.

I am reminded of the rules:

No one has the crystal ball and you will never know when the markets decide to be green or red.

A small amount of leverage is fine but not when it is concentrated into one counter. Remember to diversify but not over diversify.

Always use option to your advantage, not to speculate.

When you lose to the market, blame no one but yourself because no one forced you to invest. You can keep cash and seek cash solutions but if your cash deflate, that’s on you and no one else.

With a S$10k portfolio, I would split it up into a few tranches.

Robo Advisors

Robo Advisors are a great tool if you do not know what to buy or when to buy. The whole idea is to buy when markets go up or down. The entry level for robo investing is so low that anyone can invest. Let’s also be real, all platforms have a cost upkeep so fees are unavoidable. For this I would Assign at least S$6k (~60% – 70%) into such funds and this forms the Core part of the long term portfolio

The first option can be Endowus (USD ETFs) which i discussed before here at Endowus

The second option can be Stash Away (USD ETFs) which i discussed before here at Stash Away

The third option can be Syfe (For SGD related equities or the Global Equity Portfolio) which i discussed before here at Syfe

Now, you must not forget to top up your investment on a monthly basis. Treat that as a form of savings. The earlier you save, the faster your will reach your retirement goals.

From the robo advisor portfolio construction, you can choose a partial bond|equity balanced fund. This is where your bond exposure comes in. Do not waste your time with SGS or SSB during this period because they returns are not great.

Cryptocurrency

2. They say that trend is your friend. The trend now with all the hype is about Cryptocurrency. I can’t help but would add a small amount to the portfolio. They are supposed to act different as compared to fiat currencies. For this I would assign at least S$1k (~10%-15%) and i consider these as alternative asset class.

The first option is to buy Bitcoins. They are by far the largest Cap in the Crypto World.

The second option is to get a foot in to Crypto.com. I previously discussed about this as well here at Crypto.com App/

Funds

3. Personally, I like income or dividend equities or funds. If you are more risk adverse i would suggest to put some money into the PIMCO income funds. They are just the best in class for bonds. Depending on what you like, the average dividends is roughly around 3-4% p.a. For this, I would assign at least S$2.5k (~25%-35%) and these are supposed to be a stable source of dividend funds.

Trading

4. Finally, what fun is there if you leave everything in the Core Portfolio. The balance 15% of funds (~S$1.5k) can be use to buy in specific equity counters in the SGX. (for e.g. bank stocks or reits whenever there is a market pullback) If you really wish to fully invest these monies, just put them back into the Robos or ETFs.

What other options would you do or suggest to do? Feel free to comment. The whole idea of writing is to really share about opinions and you never know when an idea strikes you.

Disclaimer

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

In my earlier posts, I talked about the need for an emergency fund and other than Singlife, which caps the 2.5% p.a. for the first S$10k. No other financial institutions have been able to match this super high interest yield for a pretty risk free approach .(Given that Singlife is under SDIC so the first S$75k is covered and safe) In recent months, we have seen some insurtech or alternative ways to put your money and entice people with relatively decent interest rates for your cash/emergency funds.

Emergency Funds

To recap, your emergency funds should have some level of liquidity so that you can utilise when necessary and not be penalised for doing so. This is by far my personal first rule. It is extremely interesting and exciting to see what might happen to the digital banking sector where there is a mixed bag of consortium lining up to be licensed to offer financial services. It looks like it is going to be something similar to what these insurtech is offering or even more innovation. (e.g. bundled products, higher interest rates or even offering curated financial products, robo-advisors and payment channels) It does seems exciting to see what new innovation these services can offer and retail customers will benefit from this digital drive.

Dash EasyEarn

Dash Easy Earn is a collaborative work between Dash (Singtel payment service) and Easy Earn (Tiq – An Insurance arm of Etiqa and a subsidiary of Maybank)

Let’s go for the Pros first:

a. Flexible no lock-in period hence no penalties for cancelling the plan.

b. First year interest rates stands at 2% p.a. (So this part is locked in and low interest rate environment is set to stay)

c. Relatively low barrier to entry. With S$2k minimally as maintenance amount that you keep, you get the interest accrued on a daily basis.

d. Capital Guaranteed.

e. Interest earned can be transfer to Dash Payment Service with no extra charge and they have a suite of deals and payments which you can use to pay your bills with. There is a $2 cashback for your first Singtel Dash transaction! Sign up with the referral code DASH-RYJKN or tap on this link https://appserver.dash.com.sg:443/mgm?DASH-RYJKN now

f. You can top up anytime to this account.

g. 105% of the account value is the sum assured should something happen to you.

Now for the Cons:

a. You need to download and register for yet another app. This is the Singtel Dash App. I mean, I really hate Singtel but I will not say no to free money.

b. You have to remember to maintain at lease S$2k in the EasyEarn Account.

c. 2% p.a. only applies for the first year and I believe that it will drop to 1.5 % p.a. thereafter. (From the terms and conditions: *Guaranteed 1.5% p.a. + 0.5% p.a. bonus for first policy year, available on a first come, first served basis) – Seems like there is sort of a cap to this.

d. There is a maximum amount to this. Once you have Topped Up to S$20k, that is the cap for every individual account. So there is this element of troublesome to remember and track for a 2% p.a. but if it suits you, then by all means go ahead.

e. Here is the key part to this which you will not hear it from Dash themselves. For any transaction that you transfer out via PayNow back to your own transact or savings account, there is a payment fee of S$0.70 per transaction. This is free if you transfer to Dash payment as described above for Pros point (e).

Seriously

To some, the S$0.01 is money which they refuse to let go of but to others, not so much of a great deal. Don’t be penny wise pound foolish or you will never see the bigger picture. You will not gain anything by spending time and energy on pinching 1 cent. I personally know 8 out of 10 people does it and it annoys the hell out of me. If you have time to pinch 1 cent, I would rather you take that time to find ways to make $10 instead of ruining your own mood, wasting your time and fussing over the small things. I don’t get it and I still don’t today.

The User Interface

Here is how the screen looks like on the Dash EasyEarn App. You can see the Grow Money (New) in the Dash App which you can access and see your funds and interest. Do note that the interest are not accumulative though so it means that whatever you have in excess of S$20k earns no interest.

When you log in to EasyEarn, that is how the app looks like below.

Conclusion

Before I end off, I saw an interesting product which is on similar terms as Dash EasyEarn. They are from Tiq Insurance – meaning GIGANTIA but this works in their own Tiq App. (First year 1% + 1% p.a.) I’m not too sure why they have something similar to Dash EasyEarn. There can be a variety of reason. It could be that they have extra tranche of funds to offer customers or it could be that this is a longevity version of their product as compared to having inflexible Dash systems. I would explore Tiq option as well but let’s see what kind of proposition it makes to consumers.

This is not a sponsored post. This is just a tool and exploration to find out cash solutions, interest rates as well as a market survey. It is never too much to learn and know more about.

This picture image was taken off Singtel Dash and EasyEarn for illustration purpose only.

Roughly about three months ago, I made the call to go with Endowus to try out the Robo-advisor. I must say that I did and still having a good experience with them. I guess it is time to let people know that they are a dependable and competent group of people whom you can trust your money with. They also have a bunch of good content, the only thing is that their video content always over run but it just means that they have too much to talk about.

They are also one of the first robo-advisors to allow CPF investments into the funds and that tells a lot about this company. Of course, the investment funds that they use to build the portfolio is different for the Cash or SRS options which uses the competent Dimension Funds which used to be only available to institution clients (Meaning big corporate and deep pockets could only access to these funds)

Fund Fees

Now, Dimension Funds are available to retailer clients like anyone else on the street. The problem is that most places actually charge you a trailer fee, platform fee, recurring fee on top of the management fee and upfront fund fees. Yes, it is the financial industry. Endowus actually rebate those fees so that they only charge what they should be charging – the Fund level fees.

Something that really like – Endowus will only charge you fees at the end of the quarter. Comparing an upfront fee or taking a fee after your portfolio actually returns something. I would choose the latter. Don’t get me wrong, i am agreeable to paying fees and it is necessary to keep good companies running. In general, fees are the ones which keep your investment returns compounded at a lower rate.

When to Invest?

In my previous articles, i discussed about the best time to invest and frankly there isn’t any. To get a head start, the best time is really to plonk in some money to a diversified asset class when the markets have come off. Simplifying things, if you only invest 10% of your Networth each time there is a correction. Doubling the portfolio just means roughly about 9% of your portfolio. (assuming it doubles) So, it is something worthwhile to think about the risk and rewards. It also doesn’t mean that higher risk will eventually give you a higher return. In all conditions, the nature of things is that by taking a higher risk, you should get a higher return.

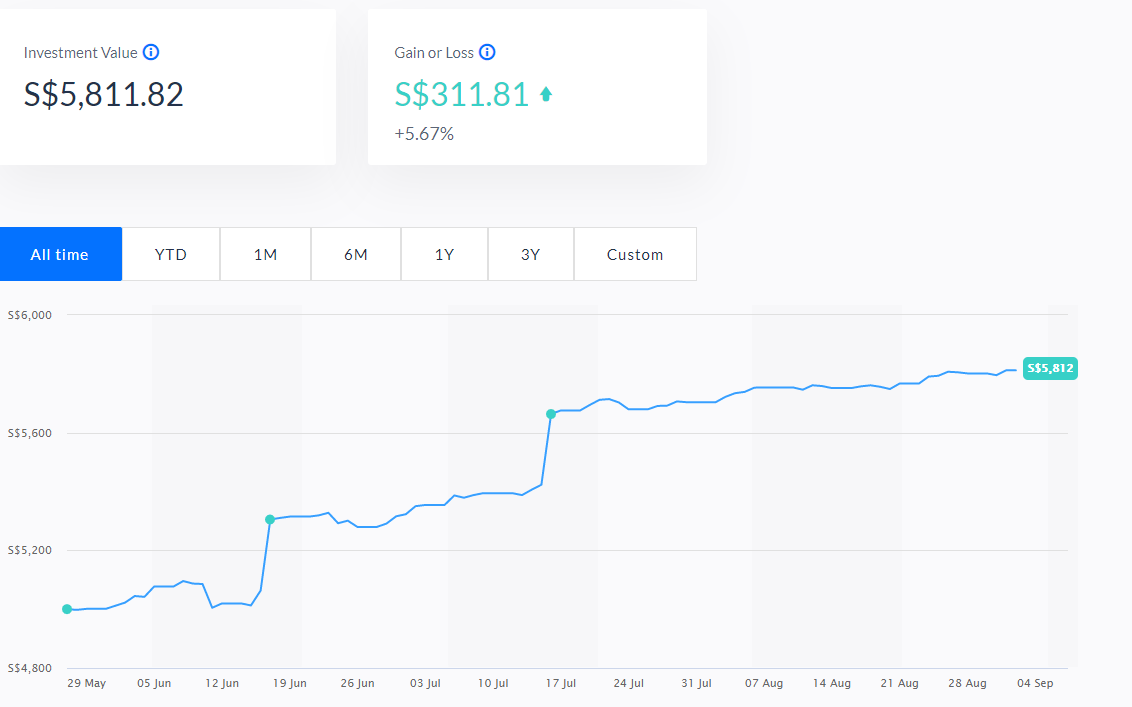

Portfolio

I had split up my portfolio into two parts. The first – A S$5000 SRS portfolio invested since May 2020. The second – A S$5500 CPF OA portfolio invested since May 2020 and YTD the returns have been pretty decent.

Figure one below is the SRS portfolio:

Figure two below is the CPF OA portfolio:

If you use my referral code to sign up and invest minimum S$10k, we both get $20 each which can be used to offset the management fees to keep their lights running: https://endowus.com/invite?code=EDZ8M

Disclaimer

This is not a sponsored post. I will still add on more of my CPF OA money regularly. I will definitely pick up more when markets come off to add on to my portfolio.

Whenever we touch on the topic of CPF, also known as Central Provident Fund (Pension Fund – The Europeans and Americans call it), people get kind of edgy and upset. What I do observe is that mostly a certain group of people is really anti CPF. The first group is those who are anti-government, not fueling anything here but just a general consensus. The second group is the retirees or about to retire folks who didn’t have a decent education (At that point in time, it wasn’t necessary to have the paper qualifications) and the last group is the self-proclaimed Warren Buffet who claims to beat the market.

The Central Provident Fund

The CPF in my opinion, is something of a great system. There are certainly flaws to it but in my view it is the perfect, AAA grade, higher yield returns that can supplement all our retirement fund. There are certain risks but There are no investment tool has no risk in reality. I finally conclude that as a result of these 3 group of people, these are the reason why so many people dislike the CPF system.

The AAA rating

a. Unfortunately, it is a complex system – You need to read up and understand how it works to appreciate the system

b. Inflation rate is here to stay hence the increase in the minimum sum yearly

c. No one is taking your money away.

d. No. There is no crystal ball. Statistically, it is proven that you can never win 100% of the time. Anyone who have tried or attempted to invest their monies will know that there is no clear strategy out there but a lot of hard work so you will not be able to beat the benchmark all the time.

e. Good quality investments and yields are hard to find these days. Perhaps it is a reality check and time to reflect about strategies as well as accepting facts and the markets

Understanding what CPF is about

When I first explored CPF, it was when I was out of school into my first job. At that time, CPF seems like a Goliath – You think you know but eventually, you slowly find out stuff which you never know before and for a long period of time I put off reading up more about them. It was many years back that I started reading financial blogs and it became like a ritual. I’ll do that almost any other day.

Back in those days, there were less bloggers so you will still need to dig deep to find out how stuff works. Then came Technology advancements, social media and super apps/content apps. I also discovered a few more bloggers who actively shared about CPF. One one those whom I follow really closely is 1M65. His is a well-known blogger for CPF and he developed his own strategies around what the CPF has been doing for many years.

Life Cycle

1M65 is really about having a million in your CPF by 65 years old. Depending on how you look at it, he is preaching a 4M65 these days and base on his concept – I do think that is possible if you start really young. Anyway, his idea about have these sum of money is really to get you thinking about your own retirement early, not just when you are in your mid stage or even late stage of your life cycle.

Everyone is different

Most importantly, everyone is different. There is no need to look at it in the form of a showboat or saying that it is impossible. Being open and understanding how these people are doing do help yourself to be ready for retirement – You are doing your next generation a favour so that they will not fall into the sandwich class or fall in the same cycle again and again. Of course, teaching the value of money to the next generation is something that needs to be worked on as well. It’s not like they were given a sum of money to deal with in life.

Some people actually worked two jobs or even saved excessively so that they can put all their money into retirement. Again, lifejourney preaches about having your own quality of life. If you need to feel like you have to give up everything just to be thrifty (It is a really thin line to term it as miserly), then you would most likely have to re-think your strategy.

The Practical Approach

There are a lot of concepts that you can read about but most of them come from a theory. Personally, I don’t really like to dissect those as they are so technical and heavy. Most importantly, it is extremely boring to put them down in words and executing them is really the best way to practice

Stock market digital graph chart on LED display concept. A large display of daily stock market price and quotation. Indicator financial forex trade education background.

As 1M65 says, you can hate who or whatever but don’t hate free money. Initially, it sounded like a money grubber statement but eventually I came to realise that, it is really free money. If you have no plans to be an entrepreneur, there is a few things you have to take note of in CPF. Yes, I am sorry but everything has to start from the basics.

My View on CPF

a. My biggest take on CPF is to compound the interest. The more you have, the greater the growth. The younger you fill up your CPF account to accumulate interest, the faster and bigger your pension fund will grow.

bi. If you are below 55 years of age – Your first $60k in CPF will gain an extra 1% p.a. (This is capped at S$20k in your OA) The current base Ordinary Account (OA) is 2.5% (3-month average of major local banks’interest rates, whichever is higher)

bii. For most people, the next S$40k will most likely be in your Special Account (SA). For others who are still building your SA, that will be whatever that is in your MediSave Account (MA). The base rate for your SA and MA is at the current floor of 4% p.a. (which is also the 12 month average yield of 10-year Singapore Gov Securities – 10YSGS)

My Tips:

Your CPF interest is computed monthly based on the lowest balance for the month. This means that for interests paid out on your CPF accounts in Year 2020, the interest amount is based on what was captured monthly, compounded and only paid out to you in full before 1st Jan of 2021.(This is subjected to changes if you have transactions every month)

c. As much as possible, you have to try your best to hit the minimum sum as early as you can. (Combined OA and SA) Once you manage to do that, you do not need to worry about the annual increase in minimum sum that is subjected to inflation.

My Tips:

Don’t lose faith if you have not or still very far from this. Everyone starts from $0. Let the small actions and do up your checklist one by one in order to build the financial confidence. Everyone is different – it is the end goal that matters.

d. Depending on your circumstances, you can choose to invest your CPF OA money after the S$20k accumulation. Similar to cash, have a long term goal and build your portfolio. Good companies and investment ideas doesn’t come easy. You have to make sure what you invest is more calculated risk. There is a risk to everything.

My Tips:

Don’t be affected by market noise. My tip is to buy when there is a price drop if the investment moat for the company still makes sense. (but always do your own diligence) You can also have different pockets of funds so that when there are opportunities or if there is a correction, you can be ready to enter the market. The rule is to always stay invested.

Summary

In Summary, CPF is not the perfect solution but a supplement of your retirement goals. In this aspect, we are responsible for our own money and retirement. No one else will take care of your money as much as you will do. Only you will know your own financial situation. The question is to ask to meet these financial goals is that if you can cut back on your lavish lifestyle or even saving more to add to your pool of funds. No one can coerce you to do what you do not wish to.

Disclaimer

This is not a sponsored post. This is purely my own opinion about CPF and retirement. If you like what you are seeing, do remember to check them out and do your diligence. There is no one size fits all investment strategy as usual