Whenever or do we ever discuss the CPF system with friends and family. The actual fact is that I never really do unless it is time to do something about it. That involves tax season or even property tax season. I do feel that it is a system that we think we all know but once we delve deeper, there’s always something new to takeaway.

Let us also face it. It is a dry topic and a very long-term one. It tries to mimic a pension fund of some sort with some level of control yet it works differently for different people. I can understand why some people come to dislike the policy but in general, there’s not much hate around it. We also have to be factual that Anti-government does not mean you need to be anti-CPF. Some might differ but I think all tools that bring one to the final goal are the ultimate endpoint.

Contribution rates according to age and wages

The rules are pretty simple. Understanding that before 55 years of age, all employees have to contribute 20% of their gross salary. Subject to the ordinary wage cap which we have discussed previously.

After 55 years of age, the contribution starts to decrease. This makes sense since the decrease in employer contribution, older employees will become less expensive and it helps to make employment more affordable.

After 55 years of age, the OA and SA will be combined and set aside in one’s RA to safeguard a monthly payout in the later years. This is probably why the contribution rates start to decrease then. Further, with increasing age, the focus will be more on wealth preservation and income that can be utilized. That would be the next reason why the contribution is lesser as time goes by.

Contribution by age from the CPF website

Understanding the CPF – Did you know? What contributes to your CPF?

Understanding that CPF system – These mainly include all forms of payments that are paid out to the employee by the employer.

Basic Wages

Overtime Wages

Bonus

Cash Incentives

Commissions

Cash Incentives

Understanding the CPF – Did you know? What does not contribute to your CPF?

Termination/Retrenchment Benefits

Reimbursements

Benefit in kind

Disclaimer

If you like what you are seeing, do remember to check them out and do your diligence. There is no one-size-fits-all investment strategy and no one solution to life. Join my telegram group to find out more about deals and join the community to connect for ideas: Life Journey Telegram

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral Services

It is very interesting to know that many people are interested to know about the CPF. Hence, I’ve decided to do a simple part series that focuses on selected and focused information so that it doesn’t take too long to read and understand. In my previous CPF series, we discussed the increase in CPF contribution on Ordinary Wages aka Salary.

CPF is a complex retirement module indeed and it has different accounts. CPFIS in turn has its pros and cons. One needs to understand it to use it to your own advantage. Most of these come at retirement as a motivation or tax deductibles. That said, it works differently for everyone so good to be in the know. One can be anti-government but we should applaud a strong and stable governance. This in turn will relate to a trusty CPF system not everyone can replicate.

Types of CPF account and what they can do

Ordinary Account:

Be happy retiring and be happy doing what you do when you retire

Though CPF is restrictive OA is the most flexible out of all three accounts before one turns 55. This is the account that one can use to invest a portion into selected CPF-approved investments (CPFIS), gold, approved insurance, and also property payments. One can look at index investing using a Robo Advisor of some sort. such as Endowus or StashAway. Endowus ticks a little better for me for the investing portion. If we look at the iShares US index Fund S&P 500 that Endowus offers to track the S&P500 (100 years of historical performance). I also have my funds consistently invested in them and it has worked well. What I really like is that they care about who invests with them and the fees.

You can check them out here at Endowus or in my previous posts which I slowly grew to like over 2 years. Asset Allocation does not time the market and during times when I’m distracted, I do not need to log into my app to proceed with my own adjustments or take action. (These take time and effort)

Asset Allocation

Special Account:

This account builds the Retirement account that will eventually be used in the retirement account in the form of an annuity. More restrictive than the OA, it has limits and can only be utilized for retirement-related financial products (Nothing much can be done in this account) It is also known that OA can be transferred to MA – This is well known to be irreversible once you have done so. Do consider your circumstances before you do anything)

Medisave Account:

This is the most restrictive of all and as it states Medisave means it can be used for certain medical payments with a limit. The MA account is also allowed to be used to purchase medical-related insurance.

Retirement Accounts

Retirement Account:

This account is non-existent until you reach 55 years of age at the point of writing. This is the combination of your OA and SA to form the annuity payout.

There are also many ways for one to contribute to your own CPF accounts. I’ll say it is a good problem to have if you need to think of fresh ways to contribute to your own CPF funds. (i.e. self-employed and looking for proper and forced retirement). Side note that CPFs are monies that are locked away in the form of something like a trust so one can’t claim your assets in your CPF (If for some reason, you are locked up in a situation of some sort)

Some ways to look at contributing to your CPF accounts

Make cash top-ups or Top up Cash + CPF

Your OA, SA, and MA – through these cash top-ups, you can earn interest. Note that these are long-term retirement uses.

Can’t say that too many times if you want to do forced savings.

Matched Retirement Savings Scheme (MRSS)

If you’re 55 to 70 and have yet to meet the current Basic Retirement Sum (BRS), you can make cash top-ups to get higher retirement payouts. The Singapore Government will match every dollar of cash top-ups made to your RA, up to a maximum grant of $600 a year. The scheme will run from 2021 for five years for a start. (Taken from the CPF website)

Helping your parents or in-laws with the CP scheme helps you and the older folks as well.

Invest your OA savings

We discussed the option of investing in a wide range of investments to grow your retirement nest egg in the form of the CPF Investment Scheme which is very highly restrictive.

As for SA, you can invest in those too but even more restricted.

Voluntary Housing Refund

If you have used CPF to purchase your house and have excess cash. One way is to kind of payback voluntarily. However, recently the cash returns outweigh that of CPF returns so with careful management, it does seem like it is better to hold cash but it is a better yielding instrument for now.

Too complicated? Leave it as it is and put the cash via this method to earn that CPF consistent return.

For CPFIS/Investing – The reason for Endowus

Like a broken recorder, why do I like using them for now:

Endowus is the first and only robo-advisor to be approved by the CPF board.

100% trailer fees back to the consumer, not the fund management fee. This is really one of a kind I’ve seen so far.

They do have a decent team that makes sense when introducing their platform in my personal opinion.

I believe all retail investors should try them out because of how they are trying to disrupt investing and make investing work for everyone.

If you like what you are seeing, do remember to check them out and do your diligence. There is no one-size-fits-all investment strategy and no one solution to life. Join my telegram group to find out more about deals and join the community to connect for ideas: Life Journey Telegram

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral Services

Quick update on the recent spate of changes regarding bank interest rate changes. I decided to take on a review of all the interest rate reviews that I’ve picked up over time. The first of this series will be from Trust Bank. If you did not know, Trust Bank is a digital bank that is in collaboration with Fair Price Group X Standard Chartered Bank Singapore.

All right, if you have not signed up for this Trust Bank Freebie, I think it is still available now. Please do sign up using my referral code “MREC9F7G” at Sign Up here at Trust Bank

a. You will get a $10 fair price voucher that you can use when you visit any Fair Price Supermarket outlet.

b. You will get an additional $25 fair price voucher once you make your first spend on your card (no minimum spending amount) Pretty sweet, I would say.

c. On top of that, you get some perks of free coffee when you go to Kopitiam to name a few.

At a first glance, I didn’t really like the logo and branding. It does feel too corporate and dated but that is my own opinion

Next, I always believed that all new businesses should be revolutionary from traditional ones. I expect no less from digital banks. Instead of making things easy to understand, It seems like it isn’t too simple. I’m a simple person, if I don’t understand, I think most people don’t and will not bother to find out more. I don’t really know how is it like in terms of their sign up but I’m pretty sure it has stagnated.

In any case, Just see it as Bank Account and Link Point Reward for simplicity.

Bank Account

For Bank Accounts, you will get a base of 1.5% for amounts up to SGD 75,000.00 (In any case, they are also SDIC insured for up to the same amount of SGD 75,000.00)

If you spend 5 transactions on your Trust Credit Card Every month, you will get an additional 0.5% for amounts up to SGD 75,000.00 and hence your total interest is 2.0% p.a.

If you are a Union member, the 0.5% is upgraded to 1.0% and hence your total interest is 2.5% p.a.

a. You will save up to 21% (Credit Card) worth in rewards for a total spend of 350 monthly on that card other than at FairPrice Group, which is in summary

2.5% base rate (Earn unlimited savings of 0.5% on FPG groceries^ and 0.22% on all other eligible spend^^. Exclusive for FairPrice members only! Earn an additional 2% on FPG groceries^, capped at 12,000 Link points a year)

This spending on the above-mentioned has to be on FairPrice Group purchases only.

8.5% monthly bonus (Earn 8.5% on FPG spend^^^ when you meet a monthly minimum eligible spend of S$350 outside of FPG, capped at 5,500 Link points)

You need to spend $350 monthly outside of FairPrice Group spending.

8.0% quarterly bonus (Earn 8% on FPG spend^^^ when you meet your monthly minimum eligible spend for 3 consecutive months, capped at 7,500 Link points)

This quarterly requirement has to be fulfilled for 3 consecutive months, otherwise, that is a fit fat 0.

2.0% FairPrice annual member bonus (Earn 2% once a year on FPG groceries^, capped at 12,000 Link points)

Really not too sure if the 12,000 link points cap is inclusive of the link points earned a year or separate. This is why I really dislike complicated rewards programmes.

b. Up to 11% savings (With the debit card) I suppose this is for customers who are ineligible for the credit card. I shall not dwell on this. You can click on the link above to read more. My question is really that if the digital bank is to serve the underserved, then why penalise those who can afford a credit card. Also, if aunties and uncles are the targets, maybe online is not the best way to go for now.

All these may change at the end of 31 December 2022. Note that there is a cap of 12,000 Link points per annum. I don’t really like the cap on rewards. It is just too troublesome.

Pros

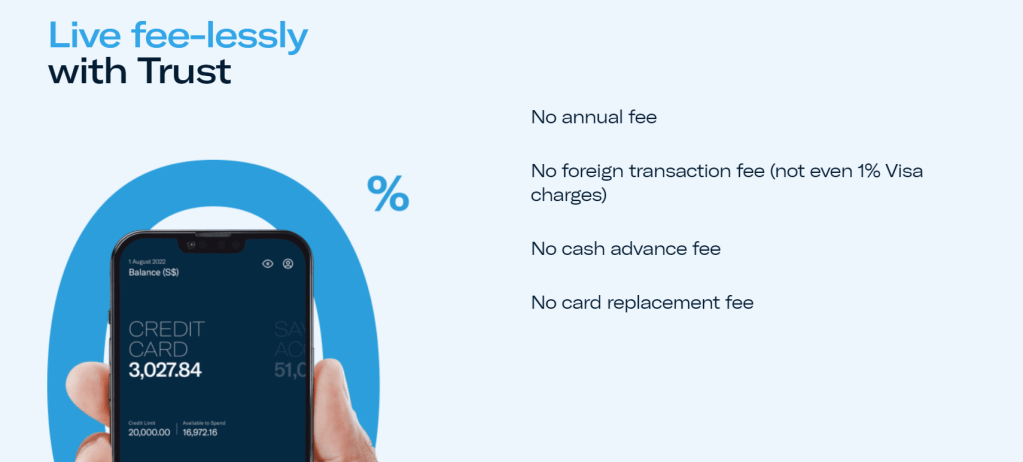

What is good is that there isn’t any lock-in period, it works just like a saving account

There aren’t any monthly fees

There isn’t any minimum balance

There isn’t any minimum period to close the account and hence an account closure fee

There’s also no card replacement fee (That’s one good thing)

Cons

Online only, not too sure about the customer service and customer care

Not sure about the service recovery

Not sure about how well they are protected in terms of security and how they manage fraud/compliance-related issues

Not sure what’s the target market.

Conclusion

Overall, it has decent rewards in terms of account-related perks and interest rates. However, I still feel like they can do more to offer a unique selling proposition. I just can’t see their deviation from their own Fair Price Group which is very local in this sense. I’m not too sure what they really want to achieve from this digital bank license.

However if it fits your bill and Fair Price is your go-to supermarket, why not? Also, If you are comfortable with online-only service as well as getting another account to remember that you have. I still think it is a 3 out of 5 stars at this point in time.

Please sign up using my referral code “MREC9F7G” at Sign Up here at Trust Bank. Thank you in advance for keeping the lights running for this blog.