I should actually do this regularly on the monthly updates to reflect how effective this portfolio can be. I missed one month of record in Sep 2020 and hence this jumped forward to the Oct 2020 portfolio.

As you can see, the last period of Oct has been a pretty volatile US market which makes diversification much more important. I am beginning to see the benefits of using Endowus as it is a systematic approach. When i initially signed up for this in May 2020, I wanted to see how the CPF portfolio and SRS/Cash portfolio performs. Truth behold, there wasn’t any worries about market dropping off and if I should sell any tickers.

SRS Portfolio

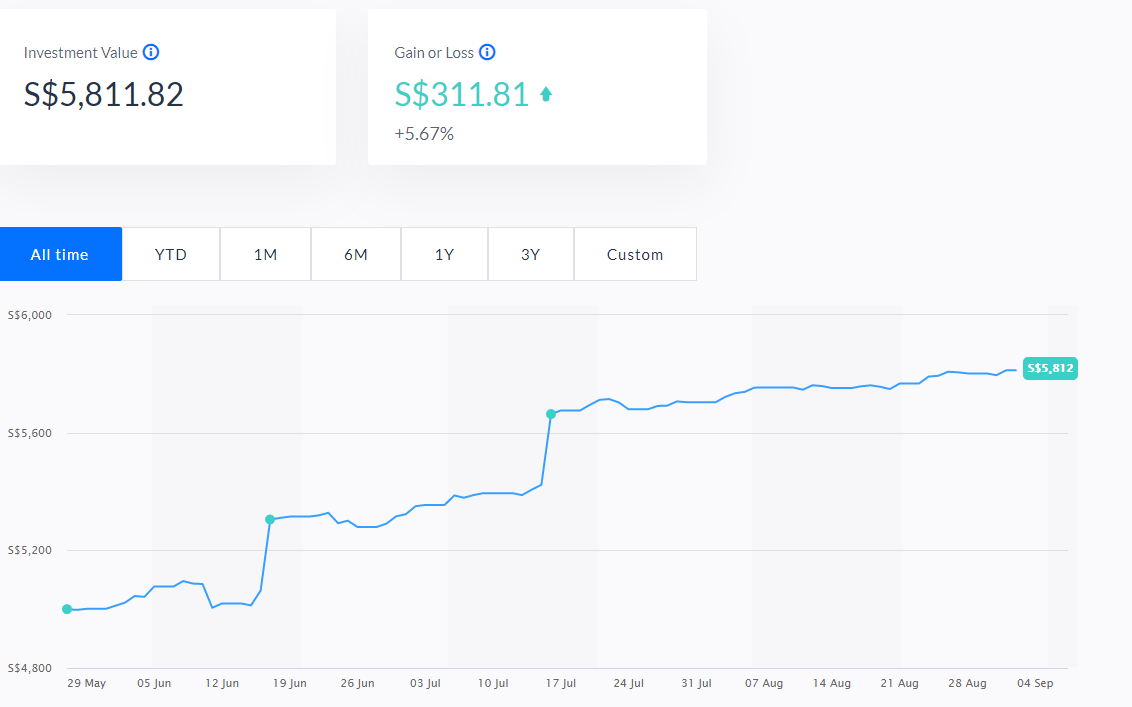

This is definitely up my alley in terms of overall portfolio management as well as long term Core portfolio. Without more talk, let’s take a look at both portfolio. This is the SRS/Cash portfolio which consists of my favourite Dimension Funds in a 40% bonds/60% equity. Overall from May 2020 to 5 Nov 2020, it is a 6.86% increase in absolute terms.

CPF Portfolio

For the CPF portfolio, it does not come with the Dimension Funds due to the restrictive nature in what you can invest in but I think this is excellent performance compared with the 2.5% in CPF.

Just simply, 6.66% in absolute returns ever since investments were made in May 2020.

Frankly, initially when I got to know about Endowus it felt like oh gosh another robo-advisor but when I started to listen and understand what they are trying to do, I am beginning to trust that what they are doing is for the good of the community and retail investors. Their fees are arguably one of the lowest in terms of value from the way i see see.

Recently they came up with a SmartFund DIY portfolio which looks really interesting. I would definitely be looking this up when there is a market pullback.

A quick review again:

Endowus is the first and only robo-advisor to be approved by the CPF board to use your CPF OA excess funds to invest.

100% trailer fees back to the consumer.

Over the months, investment content and market overview has been valuable.

Shopping for groceries, ordering food from the food apps and online shopping has taken over the world. Covid-19 has made the world to go online and digital in over a short span of time. I find the transformation amazing to the point where businesses are starting to show that they value the digital aspect of promoting their products and services. In Singapore, I do see that many businesses are transforming and redesigning their businesses to a different model as before. However, there are still those black sheep who are out there to just cheat or jack prices up to profit from scarcity.

Shopping

Speaking of shopping online. This is a really cool site to download the app into your mobile phone. This is a local company named Shopback. It gives you cashback into your account for any online spending. These days, you can link your credit card and once you spend on your credit card, the cashback automatically gets credited to your Shopback account. Talk about convenience. There is a new function that Shopback has and that is to purchase vouchers directly from Shopback. You can even use the credits from the cashback you received from previous purchases. That’s stacking more deals and more discounts.

Cashback

Each time you use your card on eligible brands and products (F&B, hotel staycation, vouchers and etc…) there will be a cash back amount allocated to you. The cash will be credited to your account ranging from 3 days to 3 months depending on when the merchant pays them for referring or recommending their products. To a certain extent, it is similar to affiliate marketing. Instead of paying out in marketing costs, the merchants pay affiliate marketers to promote their brands and Shopback gives back a portion of that commission back to the consumers as a form of incentive.

Enough said about getting more bang for your buck. Try it out and see it for yourself. We both earn a $5 bonus once you use my code and spend $20. Easy Peasy.

Save more by using ShopBack to earn Cashback. Download the app and sign up with my referral link to get $5. You can thank me later! https://app.shopback.com/OXuizVNBy9

Even More Cashback?

With the recent 9.9 sale, using a Citibank credit card seem to net you more cashback than usual. Something like additional 3% more cashback but not too sure when that would last till. Promotions don’t last forever so while stocks last. You can actually buy online vouchers from Qoo10, comfortdelgro, grab mart, grabfood, grabtaxi, pupsik, fairprice, GV and more

During random periods or campaigns, they may have upsized cashback deals which doubles the % of deals to your account once you make a transaction. From local brands to big global brands, grocery shopping and ticketing. I’ll say it is a no-brainer.

Disclaimer

This is not a sponsored post and purely my own opinion that I am writing about in my thoughts. If you like what you are seeing, do remember to check they out and do your diligence. Don’t be too fixated with what is the best.

Crypto Trading has been something that I was looking to go a couple of years ago. However the process and understanding the steps were just complex and seems daunting. The whole idea of buying crypto through a block-chain transaction and also when you transfer ETH through the ERC-20 system and so on and so forth.

I didn’t even know what was gas to begin with! Then came Crypto.com that was my initial foray into crypto currency and it gave me confidence because of how simple the setup was. It was built into 2 segments and eventually developed into a brokerage style (Crypto.com Exchange) at Exchange

Crypto.com App

The app is divided into two sections: The first is the Visa Debit Card and the second the purchasing wallet in the Crypto App. You can sell your crypto into the Visa Card (This is only one way) in the form of BTC to Fiat Currency. You can buy and sell and convert from different coins/tokens within the app itself as long as they list it in the App.

The next development that they built was the earn functions. It works like a fixed deposit. You need to put in a minimum sum, it can be no terms, 1 month or 3 month and they pay you the interest every week. The presumed interest rates are not fixed and are subject to changes. I find that the flexible terms plans allow for such flexibility. I previously talked about Crypto.com here Foray into Cryptocurrency with a Visa Card

Crypto.com Exchange

Recently, Crypto.com built an Exchange platform. This is what most people define traditionally as the brokerage. This exchange platform will allow you to set triggers for all coin pairs that is tradable on the exchange. You can also set limit buy and sell or market orders through the platform. This gives some form of control as the rates are always moving even during weekends. On the App itself, the rates are probably held for 5/10 secs depend on how volatile the trading pairs are but the exchange will provide live and almost instant conversion at the price that one would like to get.

You can also soft stake in the exchange with other coins that is listed on the page. It means that certain coins get some form of interest just by putting it on the exchange. You do not need to do anything but just take note that it may change from time to time.

Above is the referral programme for both referrer and referee for NEW Users.

They also have a referral programme now. You can also read more about it in detail here at Exchange Referral

The sky is the limit for now. Look at the referral bonus paid out in CROs Tokens. The rich gets richer.

Above is the referral programme for both referrer and referee for EXISTING Users

Benefits

No referral limits – You can refer as many friends as you want; you and your friends will each be rewarded upon meeting the requirements.

Bonus credited instantly – Referrer/Referee will receive their bonuses immediately once all conditions are met.

If you would like to give it a go or just to try it out, do use my referral code. Meanwhile, if you have any questions about funding or what to use to buy and how to buy, just drop me a note anytime.

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

Roughly about three months ago, I made the call to go with Endowus to try out the Robo-advisor. I must say that I did and still having a good experience with them. I guess it is time to let people know that they are a dependable and competent group of people whom you can trust your money with. They also have a bunch of good content, the only thing is that their video content always over run but it just means that they have too much to talk about.

They are also one of the first robo-advisors to allow CPF investments into the funds and that tells a lot about this company. Of course, the investment funds that they use to build the portfolio is different for the Cash or SRS options which uses the competent Dimension Funds which used to be only available to institution clients (Meaning big corporate and deep pockets could only access to these funds)

Fund Fees

Now, Dimension Funds are available to retailer clients like anyone else on the street. The problem is that most places actually charge you a trailer fee, platform fee, recurring fee on top of the management fee and upfront fund fees. Yes, it is the financial industry. Endowus actually rebate those fees so that they only charge what they should be charging – the Fund level fees.

Something that really like – Endowus will only charge you fees at the end of the quarter. Comparing an upfront fee or taking a fee after your portfolio actually returns something. I would choose the latter. Don’t get me wrong, i am agreeable to paying fees and it is necessary to keep good companies running. In general, fees are the ones which keep your investment returns compounded at a lower rate.

When to Invest?

In my previous articles, i discussed about the best time to invest and frankly there isn’t any. To get a head start, the best time is really to plonk in some money to a diversified asset class when the markets have come off. Simplifying things, if you only invest 10% of your Networth each time there is a correction. Doubling the portfolio just means roughly about 9% of your portfolio. (assuming it doubles) So, it is something worthwhile to think about the risk and rewards. It also doesn’t mean that higher risk will eventually give you a higher return. In all conditions, the nature of things is that by taking a higher risk, you should get a higher return.

Portfolio

I had split up my portfolio into two parts. The first – A S$5000 SRS portfolio invested since May 2020. The second – A S$5500 CPF OA portfolio invested since May 2020 and YTD the returns have been pretty decent.

Figure one below is the SRS portfolio:

Figure two below is the CPF OA portfolio:

If you use my referral code to sign up and invest minimum S$10k, we both get $20 each which can be used to offset the management fees to keep their lights running: https://endowus.com/invite?code=EDZ8M

Disclaimer

This is not a sponsored post. I will still add on more of my CPF OA money regularly. I will definitely pick up more when markets come off to add on to my portfolio.

Singapore Reits is something that many Singaporeans understand and take heart to. Some folks actually build their income/passive income via this source and I can see why.

My take on Reits on SGX

a. First it is based in Singapore – There is this local bias that it can do well given most people like to see for themselves if the malls are working out well in terms of retail quality, crowd, spending and how many shops are still in business.

b. SGD payouts avoids the currency risks. For a retiree or someone drawing on income from dividends, this payouts serve as a source of bill payment.

c. An alternative and cheaper way to enter the real estate market in Singapore is really through the reits/stock exchange. I know that people will argue that it is different but technically in my view, it is the same (And you do not need to pay stamp duties, get a mortgage and pay sales charges)

d. It is more liquid than real estate.

For a long time now, Reits have been growing big and popular within the investing community. Again, all investments comes with risks – Most people have more comfort in dealing with things they can see or get a sense of. For a long time, there have been plenty of wins for reits but as you can also see, the Circuit Breaker period in April through May have affected them in a way or another.

Diversification?

So again diversification is key to investing once more. If you put all your eggs into the Reits for passive income, then with such dividend cuts your bottom line is definitely affected. Currently, it doesn’t seem like this Covid situation is going back down or slow down whatsoever so dividend cuts is going to be prolonged in order to save businesses and jobs. Then again, there are certain sectors who might see a booming business such as Data Centres or even certain suburban reits. Sub-urban malls are definitely crowded but the former shopping aisles in orchard and high end malls are definitely missing the tourist crowd which rakes in the cash and spending. It is no wonder why people are worried about their livelihoods.

It is not all doom and gloom. Sectors will emerge while some will recover. It is definitely time to pick up some if you did not have any. The idea is to really have a long-term goals when you pick a stock and stay disciplined. Once you sell it off, you may never be able to pick back the company at their valuations again.

The Passive or Lazy Choice

If you are lazy, let Robo-advisors do the trick for you. For e.g. Syfe. https://www.syfe.com/ Initially i only took on the Reit+ portfolio some time in April 2020 to test it out so that I do not need to manage the portfolio and incur those trading fees. They have expanded other products such as a Global ARI portfolio (Long term investment into equity,bonds and commodities) and Equity100 portfolio which is 100% into global Equity ETF (US and UK listed ETFs)

Auto-rebalancing

Syfe has invented their ARI (Automated Risk Investing) methodology, which is a risk-based rebalancing strategy, which changes the allocations of your portfolio according to changes in risks in the market in order to limit your losses. In short, once it triggers a certain level, the system will trigger an alert and things start to sell off to re-allocate. It also means that over the longer term, you will naturally see a better performance of the portfolio.

Every rebalancing of course depends on what portfolio you choose from so everyone is different. I personally like the idea of investing into a portfolio of reits instead of picking it on my own. In terms of fees, it depends on your investment amount with them.

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

We hear a lot of this all the time. Our parents, our friends, our colleagues and everyone. There isn’t any in my opinion. Some may beg to differ but there really isn’t any the way the see it. There is an actual science to this because it really depends on what kind of person you are. No one will manage your money better than yourself. There are three dimensions to this how I see it.

Your Life Cycle

Life-Cycle – Depending on which part of the cycle one is in, you will change the way you invest and how you want to invest. Different stages in life provides you with different perspective and capability to do certain aspects of financial tweaks. Some get a head start while other don’t but that is not the end goal. It is your objective that is key – No one should just carbon copy a portfolio or process. This is customised and should be based on your own circumstances.

How much you have to invest?

How much you have – This is really a sticky question because the real fact is that no one knows. I am of the mind that your own networth and liquidity is for your own to know and manage. Unless you own the millions that you can’t manage because time is what you need, this would apply to at least 90% of the folks out that. How much can you afford to save or take out that does not affect you paying off your bills on time depends on your financial situation. I remember when I first started out, the salary I have is for my own takings. The very first thing I did was to spend almost all of it. It isn’t smart but we all learn.

Paying yourself first

Paying yourself first is essential in building a bigger pool. The first $1k, $10k, $25k $50k, $100k will be exponentially easier with every milestone. However if you don’t start, then the milestone will not be met. Regular saving plans/investment does help in this process. Using the envelop technique is also recommended for guys who are really starting out.

Time – This is a large and essential part of everything else.

First, you need to find time and give time to learn and experience. No one grew up knowing everything, all of these lies with exposure and experience. Some gets it faster than the rest while others manages this slower. Like an exercise buddy, the journey is long but if you persist and encourage one another, it will ride for a long time.

No excuses – Is Netflix and the next PlayStation more important every other day? Educating and understanding finance takes time and effort. Even if you hate it, try it in a smaller scale model and gradually increase it over time. I can certainly say that over a time period, it will become second nature.

Second, You do not have a warchest overnight. You need to build it. No one knows when is the next drop, what is the next promising industry to go into. No one knows who is the next unicorn or donkey but through time, you will eventually find out about your own strength and sense of investing.

My four points on a good time to invest

These four points in my opinion sets the basis of what is a good time to invest. TLDR:

a. Anytime is a good time to invest as long as you have a plan and you know what you are doing

b.Do not invest more than what you require to pay your bills.

c. Start early, start young, the later you start – the tougher it is. It is never too late but the results will be less than one would expect.

d. Learn as much as you can so that you are well-equipped. Today, there are too many tools around to learn and see.

I also do understand that by saying “When is a good time to invest?” It will attract criticism as to “timing of investment”

Timing the Market?

I would also want to address this issue of timing. It does no one any good if you time the market. No one has the crystal ball.

a. Start by splitting your warchest into different portions. Be disciplined and when market drops, buy some then don’t expect these to turn unto profits overnight.

b. Keep an eye on what you are investing especially if you are buying into a company. Investing into index funds leave you to a more passive investor. We shall not talk about Core and Tactical management of investing this round.

c. Regular investing also helps. Find mutual funds or portfolios who have in-lined principles to what you belief and stick by it.

d. Remember to always review. Things change and so do us as humans during different life cycle.

Small Note

P.s. As you can see, my beliefs is as such that all things work in an ecosystem (Before it gets disrupted). Smaller efforts gives greater confidence and these translate into positive energy, mindset and clear mind. Then, this brings you to another aspect. When this Eco-system is in place, many of the things we have discussed earlier will be a second nature and you would know how to react accordingly.

My Take on Robo-Advisor

Personally I like to use some form of Robo, systematic investing such as Endowus. It also cancels out my liking of timing my Buy-in timing.

Most importantly, the cash related funds uses a big institution related fund manage such as Dimension Fund which is not readily accessible to retail investor.

They have shown that they return the rebates they receive from the fund houses instead of absorbing it to pay fees to Banks/Financial Institutions as recurring revenues

All funds invested are held on behalf by UOB Kay Hian and held in my own name so funds are safe I say.

My only grip is really about the buy time which I have no control over. By the time the markets drop, I’m not sure when my funds are invested but on the bright side, it means it is consistent and disciplined trading.

Relatively lower management fees which means more compounding interests for all. That is good news.

I also like that they only debit the management fees at the end of the quarter instead of taking money at the start. Tells a lot about how they want to be different. Say no to upfront fees.

The first Robo-advisor to be able to invest using CPFIS. I think they were also the first to be able to use SRS to do so as well. That makes one more level up as CPFIS only approves certain funds that you can invest in. This makes it flexible to invest using Cash, SRS and CPFIS.

If you use my referral code to sign up and invest minimum S$10k, we both get $20 each which can be used to offset the management fees to keep their lights running: https://endowus.com/invite?code=EDZ8M

Disclaimer

Money is not everything – They say (Who? I don’t know). Without Money, there are lot of things we cannot do. With proper money management, these will slowly go away and your mind’s will be clearer. With a clear mind, things unravel. An end is always where new things start. Be positive and do not be bound by just money.

This is also not a sponsored posts. I used it and I like what I am seeing.

Crypto.com (MCO) has been around for almost 4 years now. I have not seen any utility crypto company who has delivered what they want to deliver to consumers over the last 4 years. They are as similar if not the same as any other company with a physical product that works.

Crypto.com

My first serious foray into crypto was the MCO card introduced by a friend of my. The great deal initially was a referral fee of USD 50 for both referrer and referee. Then comes the Spotify, Netflix and free airport access (via Lounge key – Not so much now but still it is okay) all these comes in at 100% cash-backed to the card via the utility token (Used to be MCO but now it is swapped into the CRO)

For many users, especially the pioneers or even global users who have been approved in their countries to issued MCO Visa cards (Debit card), it is certainly not what was listed in the white paper but hey, it is a pretty good move in my opinion and while the Wirecard Fiasco is still ongoing, I think it is a win-win for all Crypto.com users. Some users think otherwise but I find that this is an option once more to think bigger profits which a 10x margin might be possible. Of course crypto comes with risks. It is a big risk but it should also return big as well.

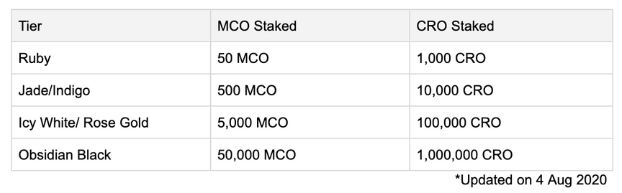

The community has been negative for such changes. I guess there is no right and wrong answer to it. I still choose to believe that is moving in the right direction for customers as well as sustainability. So in all that, I will still hold and wait on for more good news on their end. The CRO staked amount has also been adjusted lower which means more good news and more CRO released for usage.

The Swap Value

There’s the alert and actionable items: Action is required before 2 Nov 2020 at 23:59 UTC, or you will lose the functionality currently associated with your MCO. We will not perform the MCO swap on your behalf and the swap will not happen automatically.

Crypto.com will use the following formula based on the volume weighted average price as expressed in United States dollars (“VWAP”)to determine the number of CRO allocated to you that reflects each swapped MCO:

1 MCO = (30-day VWAP of MCO / 30-day VWAP of CRO) x 1 CRO

(30 days between 4 Jul 2020 to 2 Aug 2020, both dates inclusive)

So it will be fixed at 1 MCO = 27.4639 CRO

Crypto.com will offer an Early Swap Bonus in CRO if the MCO swap is performed before 2 Sep 2020 23:59 UTC, based on the following formula and criteria: So Swap early for

1 MCO = 33.1726 CRO

The pros is now that the stake and interest has now increased as CRO terms are on better rates. Development of De-fi is on its way. More flexibility in terms of usage and managing the tokens. Benefits are better now for existing customers.

The cons would be the way they initially managed and wrote on the white paper. This definitely lost some points as well as how MCO was originally the golden boy which has turned obsolete now.

All Benefits remains the same and on the same tier. Not bad I supposed, just that the quantity of CRO is now much more than before. I don’t think that’s a big deal. The whole idea is adoption, more utility and more users. It spells 10x to me more. Just be patient.

This is really a great piece of marketing work from Singlife. Though late into the referral game, this is some good way to get and garner new acquisitions. It is well known that Singaporeans are pretty starved for yields. This insurtech firm is one that I have wrote about recently and it is a good product.

(Updates 1 Nov 2020): I received an email from Singlife communications – As a heads up, Singlife Paid Referral Programme will come to a close on 1 November 2020.

All referees (i.e. people who have been referred) who have successfully in-forced their Singlife Account by 1 Nov 2020 will have up to fifteen business days (i.e. 20 Nov 2020) to order and activate their Singlife Visa Debit Card for both you and your referee to still qualify for the S$10 referral bonus.

You also probably received an email from them on 30 Oct 2020 notifying of the upcoming termination.

As from their excerpt:

“Singlife’s Paid Referral Programme has enjoyed a successful run and will come to a close as of 1 November 2020. Thank you for all your support! Upon the Effective Date of Termination (1 Nov 2020), all referees who have successfully in-forced their Singlife Account(s), by the Effective Date of Termination, will have up to fifteen business days (i.e. by 20 Nov 2020) to order and activate their Singlife Visa Debit Card to qualify for the S$10 bonus.”

Still, the good and bad and them. It is still a decent alternative cash source.

The Good about Singlife

I’ll have one more strong and valid point to date with this referral scheme.

A referral fee of S$10 is deposited in your Singlife account for each friend you invite to Singlife and there are no cap for this. Each friend gets S$10 too so if you find this useful, do use my link to sign up here: https://app.singlife.com/S49MSfXlF8

SDIC covered

Relatively high interest rate for the first $10k

Simple and fuss-free – registration and login all done online

You can also spend normally like what a debit card does, having a functioning physical card.

Transfers are all ifast which is really impressive and same day receipt

Customer service is pretty responsive and quick to reply (Live chat and email)

Some form of insurance is complimentary including retrenchment insurance (It’s not a lot but it is a nice gesture)

This is really a quick kill for a good deal. It is the usual way of spending money to get more users. This is pretty straightforward and it is an easy one to get. All you need is just to sign up for google pay using this link here https://g.co/payinvite/t74cf8f

All the way through 31st July2020, when you download Google Pay from this referral link, you will be able to receive a free $5 cash after performing an eligible transaction.

Referral Programme (until 31 July 2020)

a. You earn $5 once your friend makes his or her first payment using Google Pay. The transaction must be at least $10 to qualify. (or PayNow to your friend)

b. You can earn the reward only once for each friend whom you have successfully referred. There are no caps.

Once you have signed up using my link, you can then continue sharing your own referral link to as many friends as you would like. In return, you and your friend $5 cash each for each successful referral!

How it works?

Send your invite link for everyone to download Google Pay.

For invitees who are on IOS devices, they must enter their mobile number on the Google Pay page that is prompted before installing the app. The login must be the same as Google Pay to qualify.

You can insert a referral code if you have downloaded the app however you must not make any transactions on Google Pay before.

You will then earn S$5 and your friend S$5 if they make their first payment of at least S$10 on Google Pay by 31 July 2020 23:59 Singapore time and payment is successfully process. Also, assuming that it is a first time user as well as a first transaction.

At the time of writing, you can do this by linking your PayNow account to OCBC account (Currently that is the only way to do so) and make a transfer from there. This is the easiest and fastest way to get the perks.

It’s quite easy and simple to do. Although it takes a bit of an effort but I think it is worthwhile while they still have marketing expense to spare. Have fun referring! Please do use my referral link if you think this is of value to you. Sharing is caring – Cheers!

In the past, there used to be only 3 players in the telco market – Singtel, Starhub and M1. They sort of formed into a monopoly where 5.2 million people on the island will choose either of the 3 companies. All things change when Circles.life came into the picture and to be honest, it was such a game changer that almost instantaneously switched to them at the earliest time possible once my contract was up. Notably, Singtel has the best coverage in Singapore and underground but they were keen on only making profits for themselves.

After some time, all three incumbent were forced to break off from their current model into a SIM only plan. This has been really great for consumers in particular as more competition means more competitively prices plans and better customer service. Of course, the incumbent truly matched the competition and eventually I switch out to GIGA, a SIM only plan from Starhub.

The real benefits of going with GIGA means that for a basic plan,

a. S$18 for 20GB of data, 200 mins of outgoing calls, 200 SMS, free caller ID and free incoming calls and incoming SMS.

b. For unused data, you can carry over to the next month (Capped at 2x the base data – 20 GB x 2 = 40GB

c. No contract means, flexibility and freedom to cancel the contract anytime.

d. Signup is digital only – meaning you can only sign up online and use an app to access your account as well as setup your payments. They accept most major credit cards.

e. There isn’t any IDD so for for overseas usage, you would need to buy either gigaRoam (Asia Pacific) or gigaRoam (Rest of the world)

f. You would need to pay a small registration fee and arrange for the SIM card to be delivered to your preferred location. However, you can use a referral code to supplement the discount. You will get a one time $20 gigabucks off the 25GB plan or a one time $42 gigabucks off the 50GB plan if you use my code – “LhS9Ng”. The referral credit is only valid for any plans except the basic $10 GIGA plans.

The downside of using GIGA is that you can’t surf the internet while on a call (for e.g. checking for emails or stuffs while on a call however if you have your WiFi switched on, it works perfectly) but you can still receive OTP (One time Pin) while still on the call so that’s not too much of a worry.

Generally, I like the interface, colours and customer service support on GIGA. They even have a live chat function but you need to clear your cache regularly as it seems like it is stuck on my app most of the time. It is fuss-free and simply to use. I’ll say that they are trying hard to evolve and re-invent themselves. I don’t have too much faith with Singtel and GOMO so this is my next best choice.

GIGA just launched a 40GB data, 300 SMS, 300 outgoing calls at $20 for 12 months. It is still a no contract plan, just that it reverts back to $30 a month from the 13th month onward.

From time to time, they will launch limited time offers like the one above. You can visit their website to find out more: https://www.giga.com.sg/