Here comes another brokerage in Singapore – Futu Holdings and under the Singapore name “MooMoo”? Sounds kind of fishy but legit.

From their website:

Their investors include Tencent Holdings, Matrix Partners and Sequoia Capital. Sounds decent to me.

Futu Holdings Limited (“Futu”) (NASDAQ: FUTU)is an advanced technology company transforming the investing experience by offering a fully digitized brokerage and wealth management platform .

Futu was listed on Nasdaq on March 8, 2019.

Under MooMoo, they are under the Singapore branch, https://www.moomoo.com/ and from time to time they will run a promotion to fund the brokerage account to get 1 Apple share. Although after setting up the brokerage, maybe buying Futu stocks in the US stock exchange might be a good idea given their backing.

After Tiger brokers, here come another commission free brokerage mobile platform with similar functions and good promotions. It seems like the apple share promotion has ended. If you wish to sign up for those commission free perks and/or future promotions, do use my referral code here: https://j.moomoo.com/004Fsa

Currently, the promotion would run for 600 days free commissions.

Also if you fund USD 2k equivalent. there is a USD30 credit.

AutoWealth is my long-term portfolio approach. For my child’s portfolio, this is to add on over time and have a good 20 years horizon. My only gripe is that I cant measure YTD performance. Of course, there is no reason to do that expect for measurement purposes. A time weighted performance is more of an important indicator in my opinion. Just a reminder for myself and on why I chose Autowealth:

Why Autowealth?

My two reasons for doing so is really just (a) try out one more robo advisor/segregate a portfolio for a sole purpose and (b) segregate this fund for any other purpose other than the kid’s investment journey.

Don’t sweat the small things, the costs of robo are so low. We are talking about a 15-20 year horizon here so heck those low costs. You need to pay them to keep their lights running.

Perhaps Auto Wealth is in a different segment all together but they are the ones I see positively after the other two. After signing up in June, I finally got to funding the account in September and October when markets were on the downside. The idea of doing this over the long term is to really to buy in when markets drop.

Markets will go up and each time it drops, just pick some up and let the robots do the work on balancing and re-balancing. As long as fees remains low, the portfolio will grow over time and over a longer period. It should remain in the black based on some back testing. I like it that they have already breakeven so it would be less of a pressure as a company.

As a pretty new kid on the block, it does look like they are one of those companies who keep things lean, mean and transparent for others. Many times, I do not mind paying slightly more for better service or better app/products. I speak for myself though as I do know many who penny pinch and I shall not comment more on this. My philosophy is to never sweat the small stuff – To have bigger dreams, you will have to let go of the small things. No change in Portfolio allocations.

Performance – Feb 2021

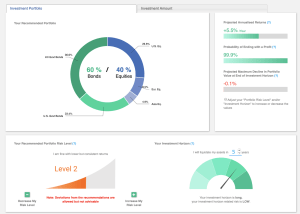

Looking at the portfolio, it is pretty expected as the market has been pretty neutral. My investment horizon would be estimated to be 15-20 years. This is a portfolio which is set at roughly 40% equities and 60% bonds. The investment vehicles will be through ETFs. It does look like it can withstand long term peaks and troughs. What i really like is that i can switch between the SGD and USD currency performance portfolio as well as the impact on USD SGD forex on performance. USD has been steadily increasing versus the SGD.

Overall, since funding to date (in SGD currency) performance is +9.13% and I like this. The impact of USD on SGD is about -2.08% and by referencing the portfolio in USD, absolute return would be at +11.00%. No complaints thus far.

Looking into the details if I were to look at the portfolio value at $5334 (end Dec 2020) versus today at $5457. Some simple and manual YTD calculations below

YTD Performance[($5457-$5334)/$5334] x 100% = +2.30% (YTD 10 March 2021)

Disclaimer

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

If you like what I am sharing or if it resonates with you, do use my referral codes here at Referral and Recommendations

The pictures were taken from Auto Wealth website for this article. If you need a referral code, drop me a message and you can indicate my full name during registration. From there, both of us will get $20 each to supplement the fees.

There are many times when we are angry. Be it for the right or wrong reasons, there will be times where our own limits are being tested. Some people just cannot take it that they are wrong, that’s just more Alpha kind of folks. Some people are just generally angsty all the time. The slightest thing piss them off. However, when you are angry, who is it that is really affected? Are you venting to the person beside you though you are not angry at them? Or are you just shouting to yourself for someone else you are upset about?

The person whom you are shouting and angry about probably don’t even know. So, what is the point in getting angry. I get it, sometimes i need to let off some steam too but not all the time though. The other day, there was an angsty driver who couldn’t get on the main road because there were just too many cars. The other day, I heard someone banging the table downstairs while working from home. Shouting eventually came on and I could hear someone else shouting back.

Deep Thinking

That made me think a little deeper. When you are angry, the person who do not know you are angry at them. Should you really express it? Eventually, the question to ask is that if one can control their emotions. Not me I would say. I am human and I cannot control over worrying, being angry and also overthinking. I’ll say most of us tend to think that we are right but is that really true? Truth be told, that little arrogance sometime annoys me a little. All we need is just to keep our heads down, be humble and learn along the way. There will always be someone or something that is better than you.

Investing the same?

Similarly, your investment style differs. Emotions run wild in those events and each time you think that markets are coming off, you actually risk missing a chance to recover more than what you should have if you would have chose to do nothing.

The thing about personal finance is that whether one has just starting building your finances, middle stage of building your fund or at a late stage of taking on your retirement funds. Young, old, poor or rich in all categories – There is really no one size fits all and regardless if you are famous or not. There will be emotions involved in all situation.

Recently, I also fell ill and because of that I had to take some matters off my hand. At the same time, markets doesn’t care if you are ill or well and that kind of struck a chord that I need to do less of trading and more of passive investing. Looking back at some of the portfolios for 2020. All 4 robo-advisors returned double digits which is by far the best I have seen. Of course, trading returns have been the best returns for me but those are super high risks.

Robotic in Nature

The idea in letting someone trustworthy to manage your funds are hard to come by. Banks are driven by profits and their pockets matter more than what money you have. Even if they did, they would have another agenda. Nonetheless, the idea – You get it! Only services make revenues.

Convincing Strategy

I’ve been convinced by the way Endowus and StashAway have been working for me as a portfolio:

Fee wise it is always all inclusive.

ETFs or Fund investing has always been the way to invest regularly. They track index and replace those companies who underperform along the way.

In particular, Endowus provides that 100% trailer fee rebates. It is the best one I’ve seen so far to not take a dime that is not transparent to the consumer. On a side note, your funds are in your own name (invest and managed via UOB Kay Hian but through your own channel) If anything happens to Endowus, your money is safe in that sense.

Such portfolios are not timing the market and look further into the long term. You need to be disciplined in that manner.

I mean especially for Endowus, they charge you a small fee which keeps them running. They invest into some fund types which are institutional in nature. Layman, it means as a normal consumer – you probably could not access these funds.

Usually but not always, the so called “hidden fees” are reduced due to economies of scale (Institutional class – Imagine Sovereign wealth funds)

Special corporate classes which have a minimum to invest. By using Endowus, collectively as retail investors normal retailer investors can put their money in at a fraction of the cost.

Agree to Disagree

Some points I kind of read and agree but disagree:

Yes, I read and heard that you can mimic trades and portfolios but my question is that if you have the economies of scale. How big are your trades?

Forex Exchanges rates especially in USD. Can you really accept using another channel to make the exchange or accept the market rate in your brokerage?

Replacing and re-balancing your portfolio. I think time matters more to me than doing these stuff which is time consuming. There are people who love doing this and do not mind doing so. So, leave it to those who does the best in their jobs.

This image was taken off Seedly and taken as a reference. Frankly, minimal investment amount should be the last thing on your mind. Fees, rebates and what is the company trying to achieve should be the top priority.

a. Use my Endowus referral link and both you and I will get $20 credit to our account: Endowus Robo-Advisor to sign up now.

b. Use my Stash Away referral code and both of us are entitled to a 6-month management fee waiver, for up to $10,000 SGD of assets invested. Visit Stash Away Referral here to sign up now.

The sound of Everest Gold is not exactly sound and safe at first notice but they are a new digital trading platform. You can trade gold digitally now, akin to a stock brokerage account. There are a number of articles out there from bloggers and online news that talks about Everest Gold.

Trying it out

To try it out, you do not need to put in any money. All you need is to use my referral code and your will be awarded 200k points which is approximately USD 20. These rewards can be used to subscribe for gold during their events.

No need for any transactions. Just make sure your details, bank accounts and everything is verified.

Referral is limited. Not sure if they will be bringing this back but in Oct 2020, the fee was 300k points which is approximately USD 40.

Referral

Use this link to find out more if you are interested at Everest Gold or use this referral code when you decide to sign up: TZLLE. Both of us will get more rewards for subscription.

History

A little dig up of the company. Everest Gold is a Singapore-based fintech gold trading form. The creation of such a service is to digitise gold trading and makes it easy for both beginner and expert investors. It is suitable for anyone who have interest in gold trading. I personally have also tested their customer service team and response is pretty decent.

Everest Gold uses 999.9 pure investment grade gold. 1kg bard are from a refiner in switzerland. You can also download them from an app and investing starts from 1 gram. From what it seems, anyone can trade and liquidate almost immediately. Physical gold assets can also be collected from their depositories by submission of a request in-app.

Disclaimer

I do use this service and by signing up as a referrer, both you and I will get some benefits.

As with all investments, there are risks involved so please do your own diligence.

I’ve not been diligent in posting my performance that i invest into Stash Away. It has been positive so far (the experience) and I’ll say it is on par with what Endowus is providing. In my own words, I’ll say that they complement each other and offer different perspective. I do trust and believe their views on certain aspects of investing and hence, SA shall be the second robo advisor that I will build a long term goal with over time.

I have since adjusted the risk index to below 20% as I felt that there isn’t a need to go all out Risk On. Having calculated risk per $ makes more sense in my opinion as news and information goes on a random rampage. Most importantly, I am invested – So if Mr Market decides to go up that is fine too. If Mr Market decides to go down, then it will be time to put more funds in. After all, it is a long game.

Retirement Portfolio A (risk-14%)

The SRS account since deposit is currently at +2.46% as on 5 Nov 2020. It’s one of those that I went in February 2020 before the crash came in March 2020. Nonetheless, I believe in the long term strategy that S&P 500 or index generally rises over the longer term so I have a super long horizon on this. I haven’t decide if I should fund more SRS monies into SA or Endowus. We shall see how things turn out.

Education Portfolio B (risk-16%)

This is something I set on a 15-18 year horizon. It is at +5.06% as at 5 Nov 2020 and I think that is a good return in my view. I have been averaging in whenever there are market dips. The risk index is at 16% and I will adjust from time to time as I do believer that by doing so, you sell some assets while buying into a new asset class based on the risk you set so in a certain sense, I can take profit while increasing or reducing my risk. Try not to touch any of those if you don’t quite understand how that works. There is some level of punting involved.

Education Portfolio C (risk-20%)

This portfolio has a shorter horizon of 12-15 years so I feel that I need to take on some risk to achieve my goals. This SA risk index is currently at 20% and will take on to be one of my riskiest portfolio. More funds will be added over time to achieve my targeted invested goals.

Conclusion

So far StashAway has not failed me in a sense that it fits in to my investing style and logic. I wish to put more into the accounts but I cant bring myself to invest when prices are going higher and higher. Instead, when things come down I find it easier to put money in.

To sign up or try out Stash Away, visit the website and use my referral code at Stash Away Referral

We’ll both get up to $10,000 SGD managed for free for 6 months which is a good deal.

I should actually do this regularly on the monthly updates to reflect how effective this portfolio can be. I missed one month of record in Sep 2020 and hence this jumped forward to the Oct 2020 portfolio.

As you can see, the last period of Oct has been a pretty volatile US market which makes diversification much more important. I am beginning to see the benefits of using Endowus as it is a systematic approach. When i initially signed up for this in May 2020, I wanted to see how the CPF portfolio and SRS/Cash portfolio performs. Truth behold, there wasn’t any worries about market dropping off and if I should sell any tickers.

SRS Portfolio

This is definitely up my alley in terms of overall portfolio management as well as long term Core portfolio. Without more talk, let’s take a look at both portfolio. This is the SRS/Cash portfolio which consists of my favourite Dimension Funds in a 40% bonds/60% equity. Overall from May 2020 to 5 Nov 2020, it is a 6.86% increase in absolute terms.

CPF Portfolio

For the CPF portfolio, it does not come with the Dimension Funds due to the restrictive nature in what you can invest in but I think this is excellent performance compared with the 2.5% in CPF.

Just simply, 6.66% in absolute returns ever since investments were made in May 2020.

Frankly, initially when I got to know about Endowus it felt like oh gosh another robo-advisor but when I started to listen and understand what they are trying to do, I am beginning to trust that what they are doing is for the good of the community and retail investors. Their fees are arguably one of the lowest in terms of value from the way i see see.

Recently they came up with a SmartFund DIY portfolio which looks really interesting. I would definitely be looking this up when there is a market pullback.

A quick review again:

Endowus is the first and only robo-advisor to be approved by the CPF board to use your CPF OA excess funds to invest.

100% trailer fees back to the consumer.

Over the months, investment content and market overview has been valuable.

Singapore Reits is something that many Singaporeans understand and take heart to. Some folks actually build their income/passive income via this source and I can see why.

My take on Reits on SGX

a. First it is based in Singapore – There is this local bias that it can do well given most people like to see for themselves if the malls are working out well in terms of retail quality, crowd, spending and how many shops are still in business.

b. SGD payouts avoids the currency risks. For a retiree or someone drawing on income from dividends, this payouts serve as a source of bill payment.

c. An alternative and cheaper way to enter the real estate market in Singapore is really through the reits/stock exchange. I know that people will argue that it is different but technically in my view, it is the same (And you do not need to pay stamp duties, get a mortgage and pay sales charges)

d. It is more liquid than real estate.

For a long time now, Reits have been growing big and popular within the investing community. Again, all investments comes with risks – Most people have more comfort in dealing with things they can see or get a sense of. For a long time, there have been plenty of wins for reits but as you can also see, the Circuit Breaker period in April through May have affected them in a way or another.

Diversification?

So again diversification is key to investing once more. If you put all your eggs into the Reits for passive income, then with such dividend cuts your bottom line is definitely affected. Currently, it doesn’t seem like this Covid situation is going back down or slow down whatsoever so dividend cuts is going to be prolonged in order to save businesses and jobs. Then again, there are certain sectors who might see a booming business such as Data Centres or even certain suburban reits. Sub-urban malls are definitely crowded but the former shopping aisles in orchard and high end malls are definitely missing the tourist crowd which rakes in the cash and spending. It is no wonder why people are worried about their livelihoods.

It is not all doom and gloom. Sectors will emerge while some will recover. It is definitely time to pick up some if you did not have any. The idea is to really have a long-term goals when you pick a stock and stay disciplined. Once you sell it off, you may never be able to pick back the company at their valuations again.

The Passive or Lazy Choice

If you are lazy, let Robo-advisors do the trick for you. For e.g. Syfe. https://www.syfe.com/ Initially i only took on the Reit+ portfolio some time in April 2020 to test it out so that I do not need to manage the portfolio and incur those trading fees. They have expanded other products such as a Global ARI portfolio (Long term investment into equity,bonds and commodities) and Equity100 portfolio which is 100% into global Equity ETF (US and UK listed ETFs)

Auto-rebalancing

Syfe has invented their ARI (Automated Risk Investing) methodology, which is a risk-based rebalancing strategy, which changes the allocations of your portfolio according to changes in risks in the market in order to limit your losses. In short, once it triggers a certain level, the system will trigger an alert and things start to sell off to re-allocate. It also means that over the longer term, you will naturally see a better performance of the portfolio.

Every rebalancing of course depends on what portfolio you choose from so everyone is different. I personally like the idea of investing into a portfolio of reits instead of picking it on my own. In terms of fees, it depends on your investment amount with them.

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

MoneyOwl is an initative from NTUC Social Enterprise. They are sort of a Robo-advisor coupled with a suite of wealth planning tools such as will writing and insurance solutions. What really attracted me is their rather simple way of investing and using Dimension Funds as part of their portfolio construction.

As a retail investor, you will most likely not be able to access such funds. When the market tanked sometime in Feb 2020, I picked a few Robo-advisor to invest into and look into performance a few months later. Almost six months has passed now and I will most likely show some of the performance in my later posts but I must say, by doing nothing much, all advisors reported positive returns as compared to my own stock picking.

Changes to MoneyOwl

Recently, MoneyOwl announced that they have lowered their investment advisory fees as well as absorbing the platform fees.

a. For Asset under management S$10,000 and below, there will not be any fees through 31 December 2021. This fee will be rebated back to the portfolio. So take note that only Cash investments are eligible for this rebate. The cash management accounts do not have these in place and your total portfolio value has to be above S$50.

b. There is an introduction fee of S$99 which is worth about S$535 for a comprehensive Financial Planning. Money Owl’s advisors will sit down with you to review your portfolio with detailed report and recommended next course of action. (~2 hours)

c. Additionally, they are introducing free financial resilience workshops to focus on cash flow management and debt management. Likely through Webinars and anyone can join in.

It is nice to see that as a partner to our national social enterprise, they are making moves to help Singaporeans. The reduced fees on investments which is one of the key points in long term investments. The more fees you pay, the more it affects your own portfolio performance.

However, they should really look into improving the interface. (for e.g. making it into an app) They also introduced a referral fee scheme or some promotional fee scheme for new sign ups. Not much complains other than that.

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.