Indeed in our world today, in this small island of affluent rich Singaporeans. Money is everything. It puts not just food in your mouth but also entertainment all day, all night long. What would you do without money? Cryptocurrency has taken a big fall along with traditional investments and the biggest news in town isn’t Bitcoin crashing down from it’s ATH (all time high lingo)

I also dabble in Cryptocurrency and at one point it made up about 20-30% of my entire portfolio. Which was amazing to be honest. It just raked on and on but I didn’t not take any profits. Instead I sink more into the ecosystem and punted for the 100x goal. Did I buy Luna? Did I do UST? No, I did not. Why didn’t I? I wasn’t too sure as well as I was playing MM.Finance and Dark Crypto Defi.

The Terra Luna Conspiracy

At one point I even pondered why didn’t I joined in the party at Terra Luna. But I had 0 holdings and I was wondering what did I miss out. Again, the 100x token. Unfortunately, things goes off in a snap this is part of the world and liquidity spiraled down to a level of pure single death tone. I’m not too sure how many people were hit locally but I do know there were plenty of suicidal comments online.

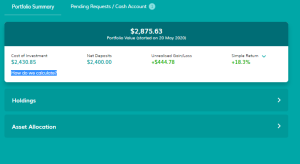

I read in many spaces that talked about having an asset allocation of not more than 5%-10% in your investment portfolio. But in that part of the space in my memory, it is just a 100% allocation into crpyto. I can’t help but feel sad to see it is down more than 50% but at least those were the profits that I ploughed in during the good times. Perhaps it is just time lost and research wasted.

Humble beginnings

In any case, It really brings back to the initial launch of why I started to note down my financial and blogging journey.

a. Don’t put in everything you can’t afford to lose when you invest. (Naysayers will say they took all the risk and became rich and that’s fine too if you made it) But I’m adverse. I have 2 young kids to feed, a mortgage and a car loan that is about to be paid up in a few years.

b. I’ve always been a bit skeptical about the all-in concept. How am I going to pay my bills for the next 6-12 months? Perhaps I’ve experienced this twice in my life. The first when I was in Secondary School where I had only $100 bucks in my bank account because I did not keep track of my spending. Needless to say, my parent’s scholarship eventually made up the bank book when I went to Tertiary.

This just proves that at a young age, it is hard to grasp the concept of personal finance. Especially when you can reach out and ask for money from your parents. This is non-existent in the World called America and Europe. Only Asian Parents do such things to spoon feed their previous child. (Laughing to myself – Who am I to say this as I also have 2 lovely girls)

My second experience of wiping out wasn’t exactly scary. It was when I got married and bought a house. Expenses were really tight and for a while, I scrimped really hard and saved on every little item.

My third experience was when I lost my job when I was 35. I had been living paycheck to paycheck. Bills, mortgage, expenses were what i needed but I lost my job. That made me think a lot. I was out of things for almost 18 months and I even tried to do a small business which put me in further financial disarray by the time I decided to pull out of it. Did I feel suicidal? I can’t deny it but I felt my existent in this world was worthless. But that thought didn’t stay long. So, for those guys who lost it all in Terra Luna, I can only say i feel you but money can’t buy you happiness.

Suicidal is an easy way out. Living is tougher. You can always rebuild but when you are gone, your loved ones will be distraught. Hence, the idea of depression can be really detrimental.

Cheers guys. I’m having a break today from work. Afternoon beer is a luxury – I understand that. My last few years were one of the greatest in a company whom emphasis is on getting things right and proper. Budget were never a budget issue. Everyone will have their day so keep on living. Don’t ever give up.

Conclusion

Health is Wealth guys. Don’t read it literally – Life is beyond just the money. Money gives you the capability and option to do many things. But life is beyond what you think it is. I can’t stress enough that when you think positive, you will get vibes and when you think you are young, you will be young.

I’m not sure how many people do read this or follow me but if what I say matters to you, it tingles with you. This is human psychology. There isn’t a need to be connected physically. When things resonate, it doesn’t need to be reasonable. You just need to know it.

It is not literal. This post isn’t about money or referral or personal finance. I feel you and many of us experienced that at least once in our lives. Just make sure that it is a lesson you learned and it doesn’t deter you from exploring options. Because, you really cannot say never to something you have not tried.

Living is more important than dying. Easier said than done but get over it and restart again. With support, it will be easier but without it will just take longer.