It’s been a while since anything kind of got me excited and Webull along with the money bull is coming along pretty nicely. During the Christmas period, there are some nice promotions to be taken away for a new Webull customer. That’s pretty sweet.

There are two items here to take note of:

There’s a time factor now for anyone who is not a WeBull customer. The promotion campaign is ongoing and running until 29 Dec 2023. Click here to sign up Webull sign-up link

There is something that is running similar to a Cash Fund promotion which doles out extra money.

Benefits of signing up

You just need to open an account with Webull, and fund any amount (no minimum) – get 10 free shares when you open a Webull account and fund any amount. There is also a Moneybull promo you can get up to US$3,000 by participating in it.

Next you have to sign up with Webull and click on the promotion link to open a Moneybull account.

The T&Cs are pretty clear from here. you can only get one of the two promotions. One point to take note of is the SGD-USD exchange rate, you have to ensure that the SGD deposited is equivalent to the USD when exchanged. Then the bonuses are tiered according to either:

Accumulating deposit with Moneybull before 29th December 2023 (3.59PM) and hold the funds until 31st March 2024 (11.59PM)

US$2,000: US$80 cash vouchers

US$100,000: US$3,000 cash vouchers

Additionally, you can put the funds into money market funds and earn the projected yields.

It is really a no-brainer to get free cash. You can also explore another app to see if it does fit with you. Never say never because if you do not try it. You will not know.

It’s been almost nine months since my last post. I am distracted a little in my new job..I’ll say that it is a job, not a career, running almost one year into this new role. I must say that I have not gotten any positives out of this but it is probably a good transition. That brings me back to my goals once more. That is to invest and build more passive income. The basics of passive income seem like that is the way to do things and remember that it is never too late to start anything.

There are two items here to take note of:

There’s a time factor now for anyone who is not a WeBull customer. The promotion campaign is ongoing and running until the end of October 2023. Click here to sign up Webull sign-up link

There is something that is running similar to a Cash Fund promotion which doles out extra money.

Benefits of signing up

You just need to open an account with Webull, and fund any amount (no minimum) – The mechanics is that you get 3 free shares.

Next, maintain the amount for another 30 days and you get another 3 free shares. That makes it a minimal USD60 for this effort. The risk Reward on this is a 5-star so it is a must-do.

It is really a no-brainer to get free cash. You can also explore another app to see if it does fit with you. Never say never because if you do not try it. You will not know.

On 4 November 2022, 3 working days after OCBC rolled out their new interest rate on their flagship 360 accounts, DBS followed up with an email that the DBS Multiplier has increased from 3.5% to 4.1%. The balance cap amount is also increased to S$100,000

The Multiplier account has always been proportioned by the transaction amount.

below S$2,000

S$2,000 to below S$2,500

S$2,500 to below S$5,000

S$5,000 to below S$15,000

S$15,000 to below S$30,000

Above S$30,000

The next layer of categories to fulfil will be the number of categories. They are known to be:

1. Salary/Dividends/SGFinDex

The Salary portion has to be a GIRO transaction with code “SAL” or “PAY”, which seems pretty strict given that there are increasing numbers of the next generation in the ‘gig economy’

For dividend crediting, these eligible dividend has to be from CDP, DBS Vickers Securities, DBS Online Equity Trading, DBS Unit Trusts, DBS Online Funds Investing and Invest-Saver (Promotion their own eco-system)

Connecting and sharing financial information from SGFinDex to NAV Planner (I would think one needs to do this on a monthly basis

2. Credit Card Spend

For the monthly card spend, it has to be on any DBS credit card and has to be eligible spending. Eligible will be the usual suspects and it will be very much dependent on the MCC codes.

3. Home Loan Installment

Home Loan financing has to be from DBS or POSB (New or Refinancing). The eligible amount will be from the monthly home loan instalment amount.

4. Insurance

Similar to my previous post on insurance and investment in these high-yield accounts. These are usually valid for a limited period and interest rates are always subject to changes. Further, only selected insurance are eligible.

5. Investment

Nothing much to comment on here. This section will be pretty hard for most people to fulfil.

Additional option: The PayLah! Retail Spend. Honestly, don’t seem like a good deal to me.

The ideal interest rate will be between 0.9% to 2,5%. Frankly, nothing much has changed though and I don’t think it is even worth announcing via their communication channels. I feel like there wasn’t even much thought placed into it. I just felt like it isn’t any effort to compete with these changes. With the most recent 0.75 bps increase by the US Feds, this is not anything competitive and not quite worth looking into for now.

The week has been intercepted by headline interest rate hike news and OCBC 360 certainly did take out their competition with a banging headline. As of the 1st of November 2022, the entire suite of the OCBC 260 flagship account will revise its interest rate across the board.

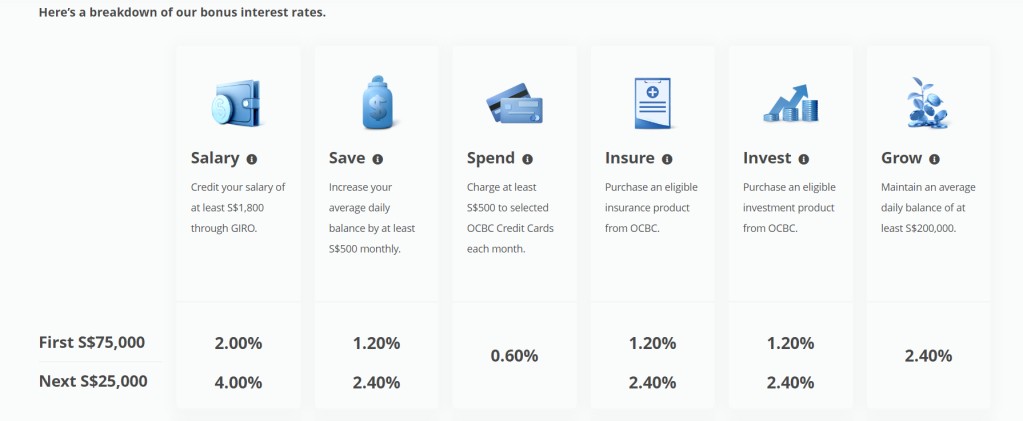

As of their online quote, “The OCBC 360 Account has six bonus interest categories – Salary, Save, Spend, Wealth (Insure), Wealth (Invest) and Grow. By tapping on just three of these categories – Salary, Save and Spend – customers will be able to earn interest of 4.65% p.a. on the first S$100,000 in their bank account.”

Prior to this due to the interest rate environment, the first S$100,000 could get you 1.85% p.a. The biggest update is that for their spending options, you can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

There are a total of 6 categories:

Salary, Save, Spend, Insure, Invest and Grow.

The basic of the high-yield account is to fulfil the following – Salary, Saving (Keeping the average daily balance by $500 increment monthly) and spending S4500 to the above-mentioned OCBC credit card each month. Quite simply put, by fulfilling these three options, your interest yield is 4.65% p.a. for up to $100,000. (technically 4.64962903% p.a.)

Over 365 days, the interest earned is S$4,649.63

Salary

You need to credit at least S$1,800 of your salary to fulfil the Salary Category. That is if your HR allows that or if you are not employed in another rival or financial institution.

Save

You need to have an incremental S$500 in your monthly balance. However, if this is your transaction account then it might be an issue. But as long as it is an incremental (Average daily balance)

Spend

You need to spend S$500 on selected OCBC credit cards. You can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

Insure & Invest

Forget about the insurance and Investment portion, there’s probably no way around those.

Grow

For the Grow category, if you have an additional S$100,000 to keep the average daily balance of S$200,000, the first S$100,000 will get an additional 2.40% p.a. while your remaining S$100,000 remain at the 0.05% p.a.

To illustrate, the interest over this S$200,000 will be S$7,099.60 hence the yield for this amount will be 3.55% p.a. (technically 3.54980161% p.a.

To calculate your interest amount, use the link to calculate the expected interest on your saving amount here: Calculate your Interest Amount

Conclusion

This is very interesting indeed. Because competitors will drastically make these changes as well. The interest rate hike might be a good and bad thing. However, take note that these rates are never confirmed or fixed. They follow the current market conditions. By taking on investments or insurance, these interest rates might change fast and furious. Overall, valiant effort and quite good timing as well. In the next few weeks, we might see revisions to compete with this increase in interest rate.

Quick update on the recent spate of changes regarding bank interest rate changes. I decided to take on a review of all the interest rate reviews that I’ve picked up over time. The first of this series will be from Trust Bank. If you did not know, Trust Bank is a digital bank that is in collaboration with Fair Price Group X Standard Chartered Bank Singapore.

All right, if you have not signed up for this Trust Bank Freebie, I think it is still available now. Please do sign up using my referral code “MREC9F7G” at Sign Up here at Trust Bank

a. You will get a $10 fair price voucher that you can use when you visit any Fair Price Supermarket outlet.

b. You will get an additional $25 fair price voucher once you make your first spend on your card (no minimum spending amount) Pretty sweet, I would say.

c. On top of that, you get some perks of free coffee when you go to Kopitiam to name a few.

At a first glance, I didn’t really like the logo and branding. It does feel too corporate and dated but that is my own opinion

Next, I always believed that all new businesses should be revolutionary from traditional ones. I expect no less from digital banks. Instead of making things easy to understand, It seems like it isn’t too simple. I’m a simple person, if I don’t understand, I think most people don’t and will not bother to find out more. I don’t really know how is it like in terms of their sign up but I’m pretty sure it has stagnated.

In any case, Just see it as Bank Account and Link Point Reward for simplicity.

Bank Account

For Bank Accounts, you will get a base of 1.5% for amounts up to SGD 75,000.00 (In any case, they are also SDIC insured for up to the same amount of SGD 75,000.00)

If you spend 5 transactions on your Trust Credit Card Every month, you will get an additional 0.5% for amounts up to SGD 75,000.00 and hence your total interest is 2.0% p.a.

If you are a Union member, the 0.5% is upgraded to 1.0% and hence your total interest is 2.5% p.a.

a. You will save up to 21% (Credit Card) worth in rewards for a total spend of 350 monthly on that card other than at FairPrice Group, which is in summary

2.5% base rate (Earn unlimited savings of 0.5% on FPG groceries^ and 0.22% on all other eligible spend^^. Exclusive for FairPrice members only! Earn an additional 2% on FPG groceries^, capped at 12,000 Link points a year)

This spending on the above-mentioned has to be on FairPrice Group purchases only.

8.5% monthly bonus (Earn 8.5% on FPG spend^^^ when you meet a monthly minimum eligible spend of S$350 outside of FPG, capped at 5,500 Link points)

You need to spend $350 monthly outside of FairPrice Group spending.

8.0% quarterly bonus (Earn 8% on FPG spend^^^ when you meet your monthly minimum eligible spend for 3 consecutive months, capped at 7,500 Link points)

This quarterly requirement has to be fulfilled for 3 consecutive months, otherwise, that is a fit fat 0.

2.0% FairPrice annual member bonus (Earn 2% once a year on FPG groceries^, capped at 12,000 Link points)

Really not too sure if the 12,000 link points cap is inclusive of the link points earned a year or separate. This is why I really dislike complicated rewards programmes.

b. Up to 11% savings (With the debit card) I suppose this is for customers who are ineligible for the credit card. I shall not dwell on this. You can click on the link above to read more. My question is really that if the digital bank is to serve the underserved, then why penalise those who can afford a credit card. Also, if aunties and uncles are the targets, maybe online is not the best way to go for now.

All these may change at the end of 31 December 2022. Note that there is a cap of 12,000 Link points per annum. I don’t really like the cap on rewards. It is just too troublesome.

Pros

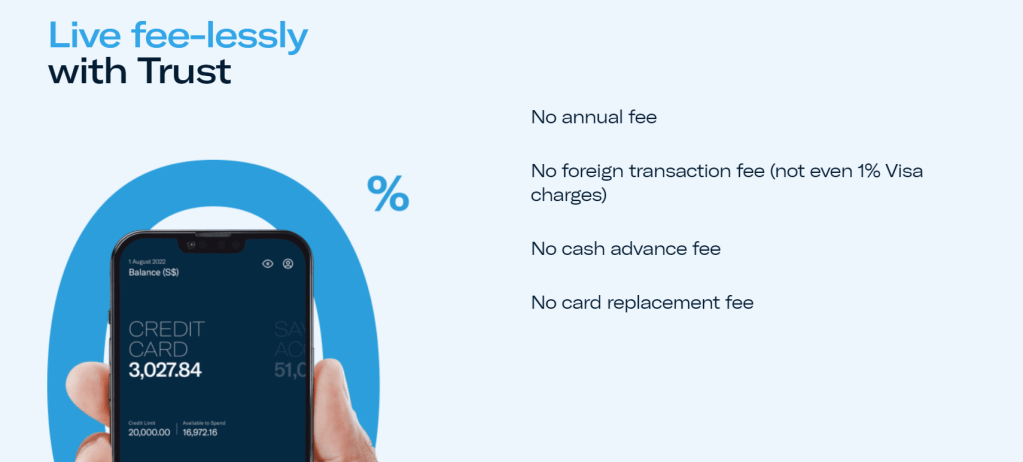

What is good is that there isn’t any lock-in period, it works just like a saving account

There aren’t any monthly fees

There isn’t any minimum balance

There isn’t any minimum period to close the account and hence an account closure fee

There’s also no card replacement fee (That’s one good thing)

Cons

Online only, not too sure about the customer service and customer care

Not sure about the service recovery

Not sure about how well they are protected in terms of security and how they manage fraud/compliance-related issues

Not sure what’s the target market.

Conclusion

Overall, it has decent rewards in terms of account-related perks and interest rates. However, I still feel like they can do more to offer a unique selling proposition. I just can’t see their deviation from their own Fair Price Group which is very local in this sense. I’m not too sure what they really want to achieve from this digital bank license.

However if it fits your bill and Fair Price is your go-to supermarket, why not? Also, If you are comfortable with online-only service as well as getting another account to remember that you have. I still think it is a 3 out of 5 stars at this point in time.

Please sign up using my referral code “MREC9F7G” at Sign Up here at Trust Bank. Thank you in advance for keeping the lights running for this blog.