Money Owl has been the regular investing strategy monthly for about close to 2 years. While the amount is nothing to be shout about. It is just regularly fixing something so that I can save and invest at the same time.

This is really a small part of my portfolio at $100 monthly RSP for around two years for now. I Probably will stick with MO for now just to compare them versus Endowus. I like the management team, honest and no conflict of interest. Maybe I add on other investment strategies on their platform if the timing is right.

Who is Money Owl?

MoneyOwl is an initative from NTUC Social Enterprise. They are a Robo-advisor coupled with a suite of wealth planning tools such as will writing and insurance solutions. What really attracted me is their rather simple way of investing and using Dimension Funds as part of their portfolio construction

As a retail investor, you will most likely not be able to access such funds (Dimension Funds). When the market tanked sometime in Feb 2020, I picked a few Robo-advisor to invest into and look into performance a few months later.

One of the reasons I went into MoneyOwl and Endowus initially was because of the Dimensional Fund. These are not readily available to retail investors but the investing landscape has changed. Retail is kind of king now.

Context

My MoneyOwl Portfolio is one that does not hold a lot. It isn’t my main Robo Portfolio but they kind of become slightly more trusted over the last few months. At the same time, for folk who have just started the investment journey, S$100 is definitely doable for a long long term portfolio. The whole idea of this blog is to also show that it does not take a lot to start building your own retirement pot. I still envy folks who are in the twenties and build their portfolio early.

However, when you are young – Money is a limited resource. As usual, personal finance also have to revolve around each individual situation and understand the situation will determine what is required.

On top of the asset that we acquire, there is a need to tweak the insurance coverage due to a new child and an increased mortgage. Should there be any issues that happen to any one of us, at least the full liabilities are covered.

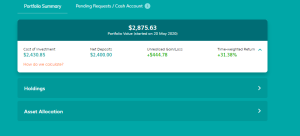

Mar 2022 performance (Day One Deposit)

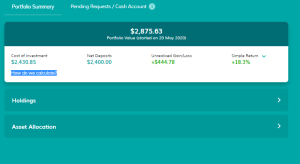

In portfolio terms, it is up +8.56% and compared to my last review in Aug 2021 which was at +18.30% on 2 Sep 2021, it has dipped quite a bit in terms of percentage points. The portfolio size isn’t something great. Just a net deposit of $3,200. I kept the regular investing of $100 per month and it’s looking rather slow. I might increase this monthly amount to build the base up a little more. 2022 has not been kind to the markets and will continue to do so. So far, the defensive nature is what I have seen as a plus point.

If we look at Time Weighted Returns, it is the more accurate to account of deposit and withdrawals at +24.63%. Again, this return is just for reference. At the end of the day, what you originally invest in and the final amount will be the absolute profit.

In terms of the portfolio allocation, there is no change and it is at 60% equities and 40% fixed income. The portfolio consists of 4 different funds. Everything will be on Dimensional Funds. I kind of wished that I had a small cap fund in there. But I guess, as long as my main robo has that exposure that would be good as well on an overall basis.

Personally, I like the allocation % because it is just widely diversified for equities and widely disperse in terms of investment grade.

In the details on the profit and loss sheet:

a. The Global Core Equity Fund will be the largest allocation and makes up most of the returns to date and continues to do well.

b. The Emerging Market Large Cap Fund will be the lowest allocation and makes the least of the returns to date. I don’t mind some EM exposure at this point in time.

c. The Global Core Fixed Income Fund will be my main steady income Fund and finally.

d. The Global Short Term Fixed Income Fund will be the last stabiliser in my portfolio.

e. The government bonds remains to be on the downside which is expected though it recovered a little as compared to the previous month. The impact is negligible.

f. Recently, the russia exposure was mentioned to investors that it was removed and likely due to the sanctions.

MoneyOwl fees

A few months ago, MoneyOwl announced that they have lowered their investment advisory fees as well as absorbing the platform fees due to the pandemic.

a. For asset under management S$100,000 and below, there will be a 0.6% p.a. management fee and 0.5% p.a. for amounts above S$100,000. This amount will be rebated back in the portfolio. So take note that only Cash investments (Wise Income will also incur management fees), the cash management accounts do not have these in place and your total portfolio value has to be above S$50.

b. There is an introduction fee of S$99 which is worth about S$535 for a comprehensive Financial Planning. Money Owl’s advisors will sit down with you to review your portfolio. The review is expected to contain detailed report and recommendations (It is estimated to be around 2 hours).

c. Additionally, they are introducing free financial resilience workshops to focus on cash flow management and debt management. Likely through Webinars and anyone can join in.

It is nice to see that as a partner to our national social enterprise, they are making moves to help Singaporeans. The reduced fees on investments which is one of the key points in long term investments. The more fees you pay, the more it affects your long term goals.

If you would like to give MoneyOwl a try do remember to use my referral code: 1JIC-91CM

Both of us with get S$20 worth of GrabFood Vouchers for every product or service that you sign up so that means that both of us will get up to S$60 worth of GrabFood Vouchers. (Total of 3 services/products)

Personally, I think that they are decent. A very conservative bunch.

Disclaimer

This is not a sponsored post. This is purely my own opinion after using their service and/or products. If you like what you are seeing, do remember to check they out and do your diligence. There is no one size fits all investment strategy.

If you would like to give MoneyOwl a try do remember to use my referral code: 1JIC-91CM

Now, if what I am sharing does resonates with you, do use my referral codes here at Referral and Recommendations

If you like what I am sharing or if it resonates with you, do use my referral codes for other services at https://atomic-temporary-178675883.wpcomstaging.com/contact/

The pictures were taken from Money Owl’s website for this article.