As on 3 November 2022

The week has been intercepted by headline interest rate hike news and OCBC 360 certainly did take out their competition with a banging headline. As of the 1st of November 2022, the entire suite of the OCBC 260 flagship account will revise its interest rate across the board.

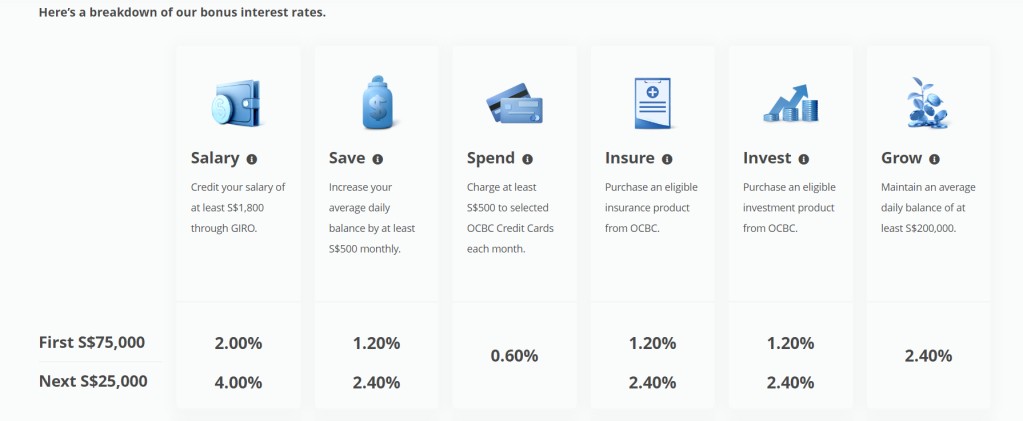

As of their online quote, “The OCBC 360 Account has six bonus interest categories – Salary, Save, Spend, Wealth (Insure), Wealth (Invest) and Grow. By tapping on just three of these categories – Salary, Save and Spend – customers will be able to earn interest of 4.65% p.a. on the first S$100,000 in their bank account.”

Prior to this due to the interest rate environment, the first S$100,000 could get you 1.85% p.a. The biggest update is that for their spending options, you can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

There are a total of 6 categories:

Salary, Save, Spend, Insure, Invest and Grow.

The basic of the high-yield account is to fulfil the following – Salary, Saving (Keeping the average daily balance by $500 increment monthly) and spending S4500 to the above-mentioned OCBC credit card each month. Quite simply put, by fulfilling these three options, your interest yield is 4.65% p.a. for up to $100,000. (technically 4.64962903% p.a.)

Over 365 days, the interest earned is S$4,649.63

Salary

You need to credit at least S$1,800 of your salary to fulfil the Salary Category. That is if your HR allows that or if you are not employed in another rival or financial institution.

Save

You need to have an incremental S$500 in your monthly balance. However, if this is your transaction account then it might be an issue. But as long as it is an incremental (Average daily balance)

Spend

You need to spend S$500 on selected OCBC credit cards. You can use the OCBC 365 credit card, OCBC Titanium Rewards credit card, OCBC 90°N Visa card and OCBC 90°N Mastercard.

Insure & Invest

Forget about the insurance and Investment portion, there’s probably no way around those.

Grow

For the Grow category, if you have an additional S$100,000 to keep the average daily balance of S$200,000, the first S$100,000 will get an additional 2.40% p.a. while your remaining S$100,000 remain at the 0.05% p.a.

To illustrate, the interest over this S$200,000 will be S$7,099.60 hence the yield for this amount will be 3.55% p.a. (technically 3.54980161% p.a.

To calculate your interest amount, use the link to calculate the expected interest on your saving amount here: Calculate your Interest Amount

Conclusion

This is very interesting indeed. Because competitors will drastically make these changes as well. The interest rate hike might be a good and bad thing. However, take note that these rates are never confirmed or fixed. They follow the current market conditions. By taking on investments or insurance, these interest rates might change fast and furious. Overall, valiant effort and quite good timing as well. In the next few weeks, we might see revisions to compete with this increase in interest rate.